“Salt is good; but if the salt becomes unsalty, with what will you make it salty again? Have salt in yourselves, and be at peace with one another.”

Mark 9:50 (NASB1995)

To Thomas Jefferson from Éleuthère Irénée du Pont de Nemours, 20 July 1803.

MISTER PRESIDENT,

As you know from my father, I am creating a large gunpowder factory in the United States for war and hunting. Modeled after the finest European factories, it is about to open. I had the good fortune of studying with the famous Lavoisier when he was in charge of powder works. Thanks to his guidance, I have been able to incorporate the most advanced practices into my factory and to add some innovations which I hope will enable America to rival all other powers in this domain…

Your very humble and very obedient servant,

E. I. DU PONT DE NEMOURS

Discover the purpose of your work and your corporation

What is your purpose in work?

- Your investment will create fresh employment prospects and elevate the socio-economic conditions of the local community.

- Promote ESG (Environmental, Social, and Governance) principles and align business practices with global standards.

What drives your corporation’s core value?

- Capture the new opportunities in the emerging market and introduce international best practices to the local specialty chemical industry.

- Expand your company’s portfolio within the Asia Pacific region.

Mosquito and the birth of the specialty chemical industry

William Henry Perkin was the pioneer of the specialty chemical industry. He was working at the Royal College of Chemistry, looking for a method to make synthetic quinine to cure malaria. He discovered the first aniline dye, the purple mauveine. He patented his invention in 1856 when he was 18 years old.

William Henry Perkin

Commemorative plaques

Source: Science History Institute 2017

Source: Wikipedia. Allen 2005

1.0 Executive Summary

Mission

- Objective: To establish a strategic investment team comprised of global specialty chemical groups, financial investors, and local petroleum groups. The goal is to create manufacturing hubs, licensed manufacturing operations, sales, marketing, and a robust business infrastructure in order to position Borneo as the premier specialty chemical hub in Asia.

- Stage 1: Invest in six key segments: Personal Care, Food, Pharmaceuticals, Construction, Electronics, and Water Treatment products, with a total production capacity of 1.8 million metric tons per year.

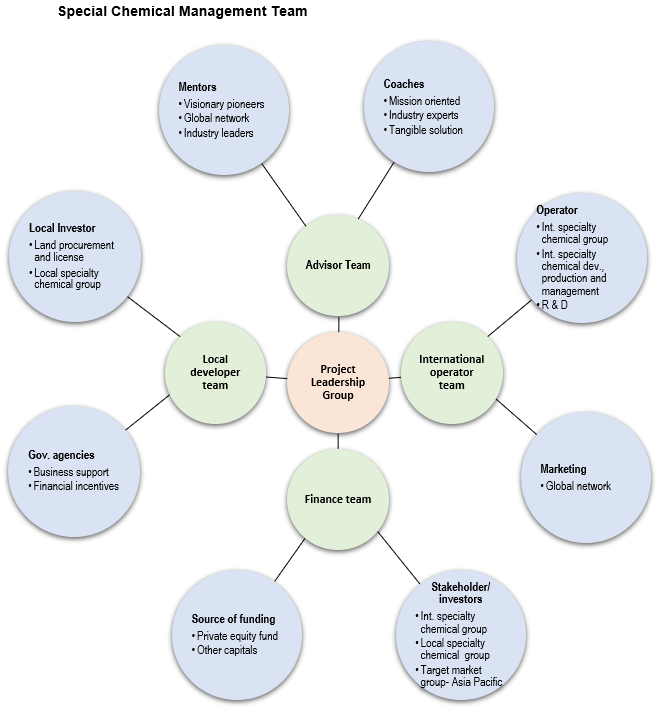

Key Management Team

- Mentors: Visionary pioneers and industry leaders with an extensive global network who provide invaluable guidance and inspiration.

- Coaches: Mission-oriented industry experts offering practical solutions to challenges, ensuring the team remains focused on its objectives.

- Partners:

- A project leadership group with a proven track record in the development, operation, and financial management of the specialty chemical industry.

- A reputable investment manager with access to funding sources within the specialty chemical industry.

- A respected local specialty chemical developer with strong procurement capabilities, a local network, sound financial stability, and solid government support.

- Target market end-users, importers, and licensed manufacturers.

Product Benefits

- Uniqueness: Specialty chemical products offer higher value-added features due to their unique characteristics.

- R&D: The industry boasts a robust research and development component, constantly innovating to meet the needs of new markets.

- Market: Emerging markets often lack downstream industries and international market exposure. Strategic collaboration with global players will help overcome these barriers.

Target Market

- Customers: Distributors and licensed manufacturers in Asia.

Financial Projections

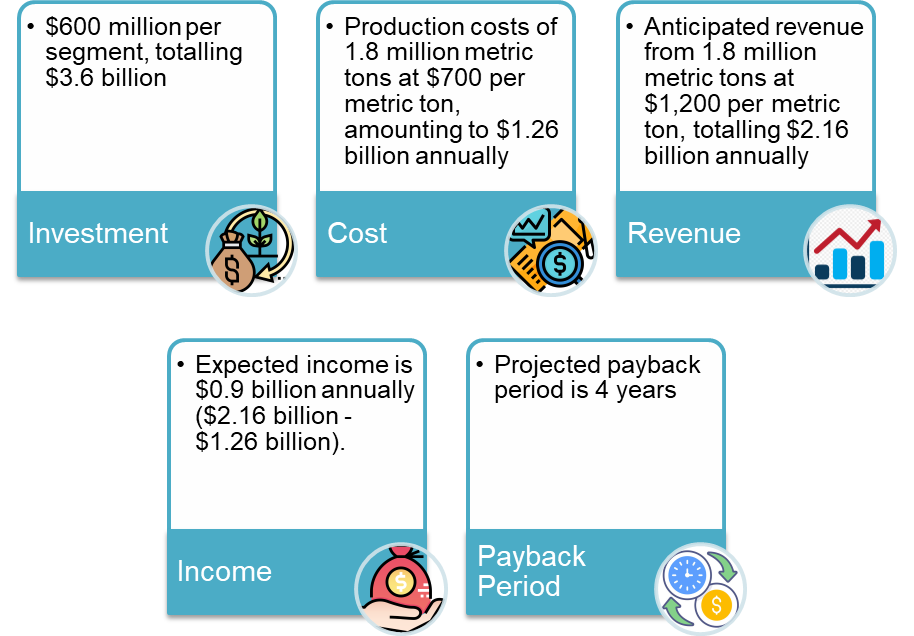

- Investment: $600 million per segment, totalling $3.6 billion.

- Cost: Production costs of 1.8 million metric tons at $700 per metric ton, amounting to $1.26 billion annually.

- Revenue: Anticipated revenue from 1.8 million metric tons at $1,200 per metric ton, totalling $2.16 billion annually.

- Income: Expected income is $0.9 billion annually ($2.16 billion – $1.26 billion).

- Payback: Projected payback period is 4 years.

Unique Business Model

- Cost Efficiency: Achieve lower production costs through vertical and horizontal integration.

- Collaborative Team: Collaboration among specialized teams will enhance performance, productivity, and financial returns.

- Market Access: Direct access to domestic markets in Indonesia, Malaysia, and Brunei will serve as the foundation for expansion into the broader Asia Pacific markets.

2.0 Mission

2.1 Challenges

- Competition: Developed nations’ specialty chemical industry faces tough competition due to low-cost entrants, regulations, overcapacity, lower margins, and high production costs.

- Value Creation: Emerging markets struggle to differentiate specialty chemical products and add value.

- Frontier Potential: Borneo has untapped oil and gas reserves but lacks investment and expertise in downstream industries.

2.2 Solutions

- Partnerships: Borneo offers competitive feedstock for specialty chemical investors in the Asia Pacific.

- Market Focus: International specialty chemical MNCs can consolidate manufacturing in Borneo, focusing on new product development.

2.3 Mission

- Entity: Establish a strategic investment team with global specialty chemical groups, financial investors, and local petroleum groups. Create manufacturing hubs, licensed manufacturers, operations, sales, marketing, and business infrastructure to make Borneo the Asian specialty chemical hub.

- Specialization: Invest in six key segments: Personal Care, Food, Pharmaceuticals, Construction, Electronics, and Water Treatment products.

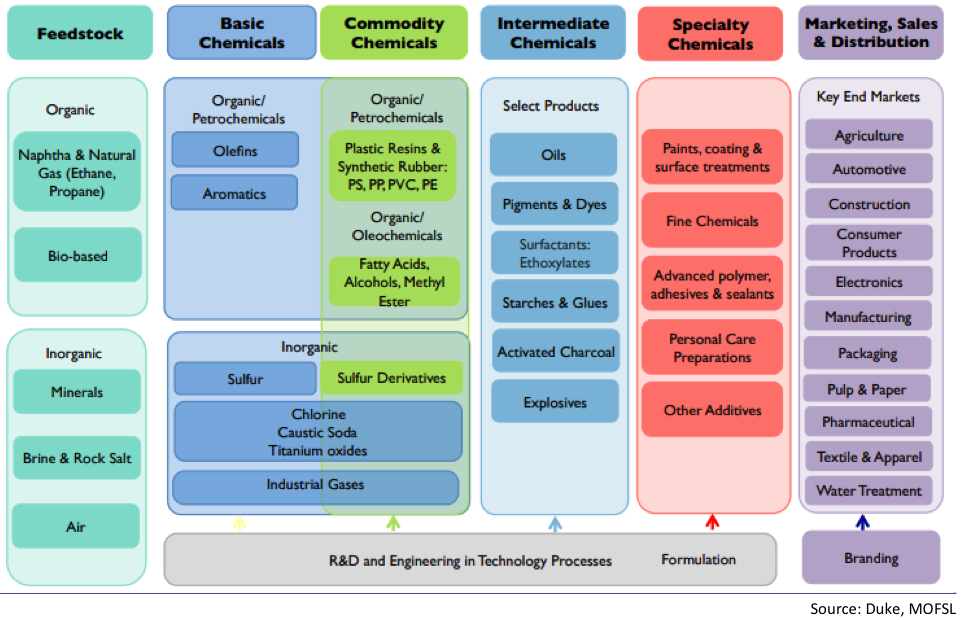

3.0 Product

3.1 Product Description

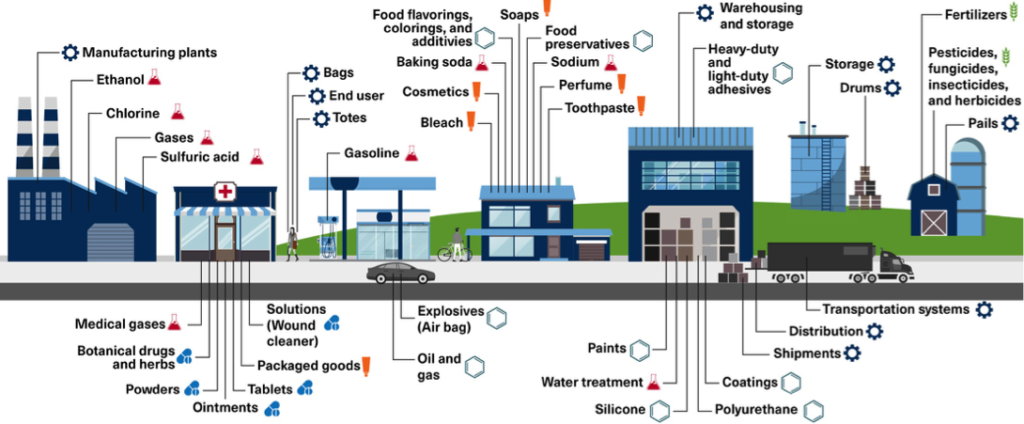

Specialty Chemicals: Specialty chemicals are performance-based products utilised in various industries such as construction, electronics, surfactants, plastics, catalysts, food, printing inks, pulp & paper, personal care, pharmaceuticals, lubrication, water treatment, textiles, and other critical sectors.

Specialty chemical applications

3.2 Product Attributes

- Specifications: Performance products incorporate unique formulations designed to enhance the performance and processing of the customer’s products.

- Innovative Solutions: These products feature innovative technical solutions within their special formulations, providing a competitive advantage in targeted niche markets.

- Flexibility: The manufacturing process for specialty chemicals is adaptable and frequently adjusted to accommodate changing customer requirements.

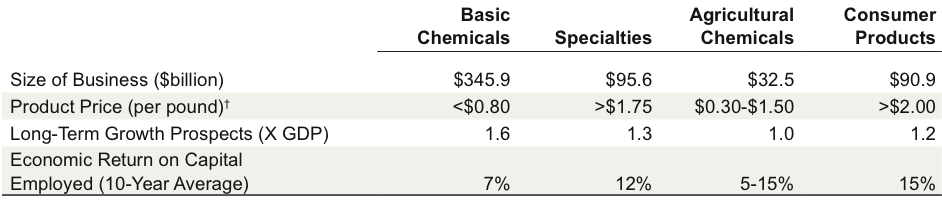

- High Value: Specialty chemical products offer significant customer and technical service components, resulting in higher value compared to commodity chemicals (valued at US$0.57/kg).

- Barrier to Entry: Specialty chemical innovations are niche-specific, protected by patents, creating substantial barriers to entry for competitors.

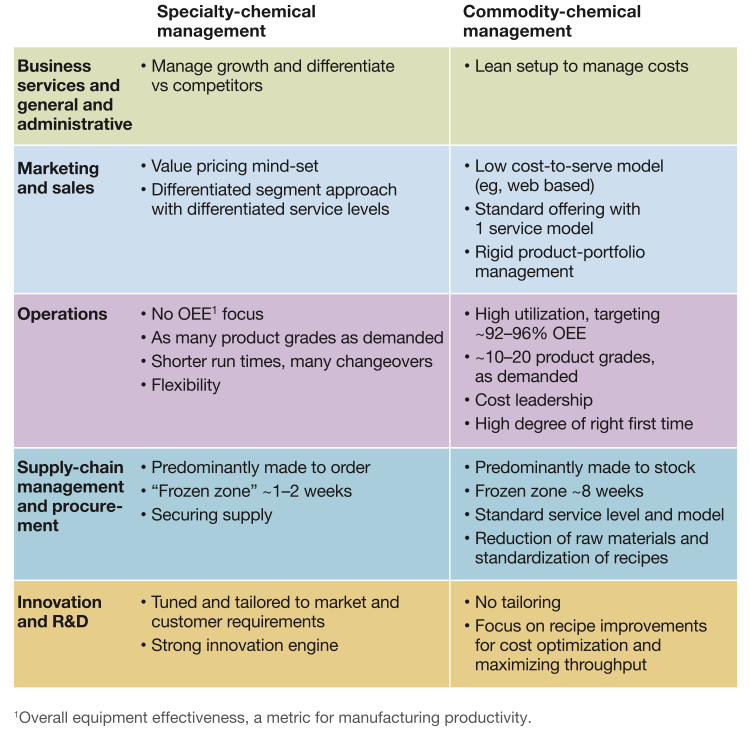

Specialty chemicals and commodity chemical attributes

3.3 Product Benefits

- Stable Income: The specialty chemical industry offers a reliable source of income.

- Uniqueness: Specialty chemical products are high-value due to their unique features.

- R&D Focus: The industry’s strong emphasis on research and development leads to continuous innovation for new markets and segments.

- Market Expansion: Emerging markets lack downstream industries and international market exposure. Strategic alignment with global players overcomes this challenge.

3.4 Product Competitive Advantages

- Cost Efficiency: Lower raw material costs, stemming from Borneo’s natural gas and petroleum product resources, contribute to higher profit margins.

- Standards Integration: By incorporating specialty performance specifications into national standards, the industry can establish stronger barriers against competitors.

- Customer Support: International specialty chemical players can seize the opportunity to provide much-needed service-oriented and technical support to Asian customers.

- Product Innovation: New product development is pivotal for catering to the growing middle-income population in Asia.

- Specialized Team: Investment partners bring top-notch expertise to the specialty chemical industry, enhancing the venture’s chances of success.

4.0 Market

4.1 Market Segments

- Segments: Four main segments – basic chemicals, specialty chemicals, agricultural chemicals, pharmaceuticals, and consumer products. Initial focus is on the specialty chemical industry for emerging Asian markets.

- Specialty Chemicals (Sp. Chem): Global specialty chemicals encompass various segments like adhesives, coatings, electronic chemicals, and more.

4.2 Target Market Strategy

- Partnerships: Establish alliances with international specialty chemical MNCs, local petrochemical groups, government agencies, and investors.

- Standards: Create national standards that incorporate specialty chemical performance and formulation specifics.

- Hubs: Expand by setting up an ingredient production center in Borneo and licensed manufacturers across the Asia Pacific.

4.3 Market Needs

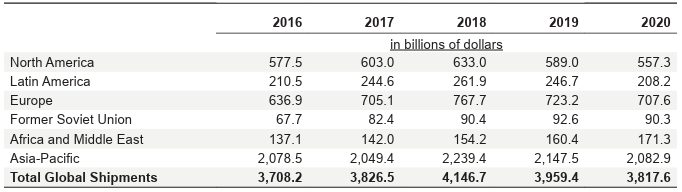

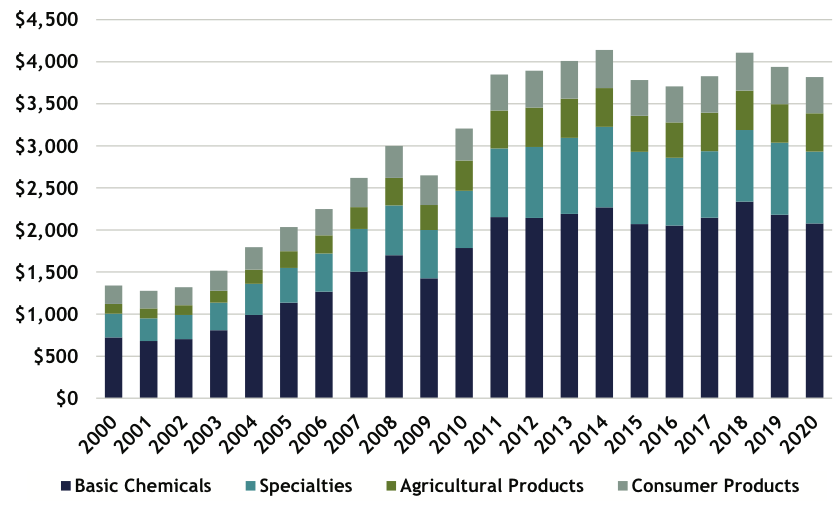

In 2020, Asia Pacific led with a US$2,082 billion turnover and US$2,065 billion in domestic sales/consumption in the specialty chemical industry.

Chemical shipment

Global chemical domestic sales 2020 (US$/billion)

4.4 Growth Drivers

- Innovation: Constant creation of new specialty chemical products fuels industry growth.

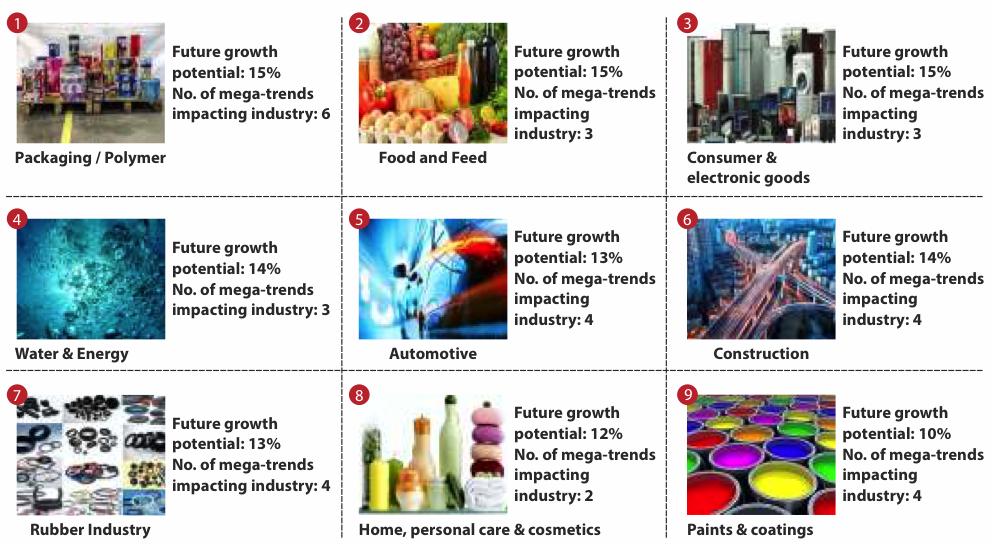

- Rising Demand: Increasing demand for consumer products in pharmaceuticals, personal care, construction, and food sectors, especially among Asia’s growing middle-income population.

- Industrialisation: Rapid industrialization in emerging Asian markets, driven by the demand for electronics, propels growth.

4.5 Key Customers

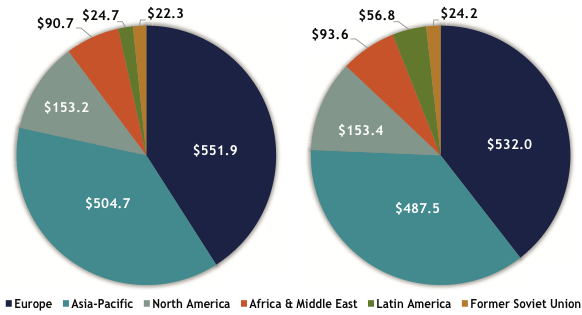

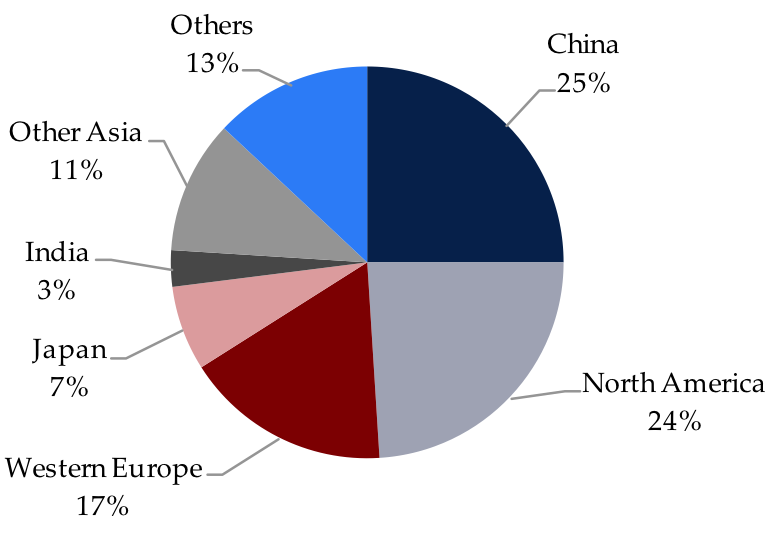

1. Global chemical – Asia Pacific is the largest consumer of special chemicals (2020)

Exports Imports

2. Global chemical shipments by segment 2020 (US$/billion)

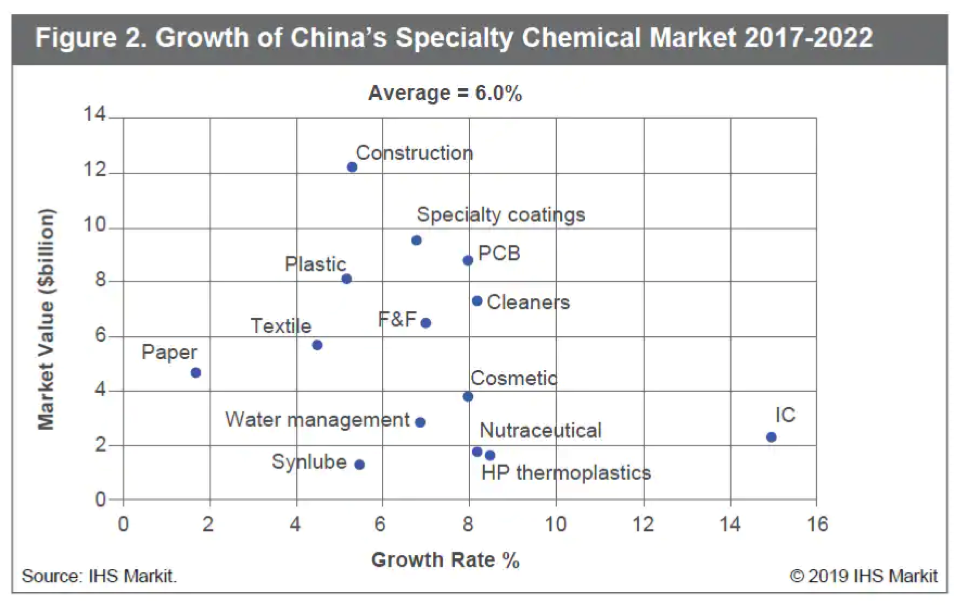

3. China – specialty chemicals growth

Key players in China:

- BCIG

- Befar Group

- China Fuhai

- China National Chemical Corporation

- China National Petroleum Corporation

- CHN Energy

- Hengli Petrochemical

- Hengyi Petrochemical

- Huayi

- Kingfa Science & Technology

- Qingdao Haiwan Chemical

- Rongsheng Petrochemical

- Shaanxi Coal and Chemical Industry

- Shaanxi Yanchang Petroleum

- Shandong Dongming Petrochemical Group

- Shandong Jingbo Petrochemicals

- Shanghai Huayi

- Shanshan Technology

- Sinochem

- Sinopec

- Shenghong Group

- Tianjin Bohai Chemical Industry Group

- Tongkun Group

- Wanda Petrochemical Group

- Wanhua Chemical

- Zhejiang Juhua

- Zhejiang Longsheng

4. Specialty chemicals end uses in India

Key players in India:

- Aarti Industries

- Aklyl Amines Chemicals

- Archroma

- Asian Paints

- Atul

- Balaji Amines

- BASF

- Berger Paints

- Clariant

- Clean Science & Technology

- Croda

- Danisco

- Deepak Nitrite

- DSM

- Fine Organics

- Galaxy Surfactants

- GlaxoSmithKline

- Gujarat Alkalis

- Heubach

- KBIL

- Keva

- Krebs Biochemicals

- Laxmi Organic

- Navin Fluorine

- Nocil

- Pidilite Industries

- Piramal Group

- SRL

- Tata Chemicals

- Vintai Organics

Key players in Japan

- Asahi Kasei

- Denka

- DIC Corporation

- Hitachi Chemical

- Kaneka

- Kao

- Kuraray

- Kureha

- Lion Corp

- Mitsubishi Chemical Holding

- Mitsui Chemicals

- Nikkol

- Nippon Kayaku

- Nippon Soda

- Nissan Chemical

- Nitto Denko

- Sekisui Chemical

- Shin-Etsu Chemical

- Shiseido

- Sumitomo Chemical

- T. Hasegawa

- Tokuyama

- Takasago

- Toagosei

- Toray Industries

- Tosoh

- Ube Industries

4.6 Competition and Industry

International key players in specialty chemicals industry:

- AkzoNobel

- Albemarle

- Arkema

- Ashland

- BASF

- Bayer

- Cabot

- Chemtura

- Clariant

- Cognis

- Croda

- Cytec

- Dow Chemical

- Evonik

- Ferro

- Formosa Plastics

- Huntsman

- Ineos

- Kemira

- Lanxess

- LG Chem

- Lotte Chemical

- Lubrizol

- LyondellBasell

- Mitsubishi Chemical

- Novozymes

- Rhodia

- Sabic

- Sinopac

- Wacker

- W. R. Grace

Local key players

- AGC

- Alkindo Mitraraya

- Asahimas Chemical

- Ashland

- Barito Pacific

- Citra Kimia

- DoveChem

- Eternal Buana (EBCI)

- Luxchem

- Pertamina

- Petronas Chemicals

- Polygel Brunei

- Royal Chemie

- Tunas Resin

- Zekindo

Market share of specialty chemicals

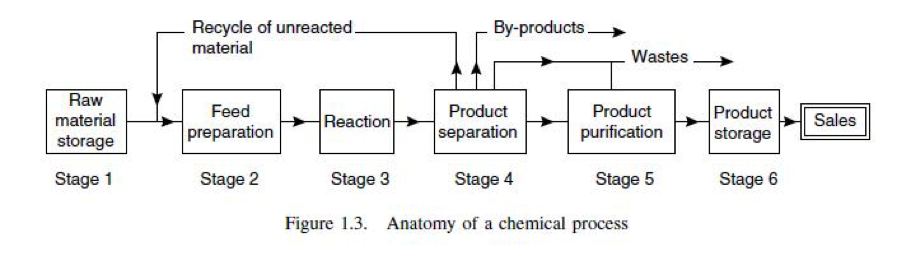

5.0 Operation

5.1 Chemical industry business operation stages

5.2 Chemical value chain

5.3 Production process

6.0 Financial Implications

6.1 Investment Segment

- Criteria: Investment decisions are based on customer needs, financial returns, and growth potential.

- Segments: Investments are allocated across six segments: cosmetic additives, electronic chemicals, flavors and fragrances, food additives, plastics compounding, and water management chemicals.

Investment

• Capacity: Each segment is designed for a production capacity of 300,000 million metric tons per year. • Investment per Segment: Each segment requires an investment of US$600 million per plant. • Total Investment: The total investment across all six segments amounts to US$3.6 billion.

Case study 1: USA plastic industry plant construction cost

Case Study 2: Indonesia Lotte Chemical Cracker Plant, Western Java

- Production: This plant in Western Java, Indonesia, produces 1 million tons of ethylene, 520,000 tons of propene, and 250,000 tons of polypropylene annually.

- Budget: The project had a budget of US$3.9 billion, indicating a substantial investment in the facility.

Case Study 3: Malaysia Petronas Chemicals Group’s Acquisition of Da Vinci Group

- Acquisition: Petronas Chemicals Group, based in Malaysia, acquired Da Vinci Group at a price of US$182 million.

- Annual Turnover: At the time of acquisition, Da Vinci Group had an annual turnover of US$195 million, highlighting the strategic move by Petronas to expand its operations through this acquisition.

6.2 Production Cost

The production cost for a total capacity of 1.8 million metric tons is calculated as follows: • Production Cost: US$0.70 per kilogram (kg) • Total Production Cost: 1.8 million metric tons X US$700 per metric ton = US$1.26 billion per year.

Case study 1: Chemical industry gross margin 2021

Case study 2: US – Margins of chemical industries

Case study 3: USA plastic industry production cost (2016) module: 16,000 m2 / 225 workers

6.3 Price and Revenue

With a price of US$1.2 per kilogram (kg), the annual revenue for a total capacity of 1.8 million metric tons is calculated as follows: • Revenue: 1.8 million metric tons X US$1,200 per metric ton = US$2.16 billion per year.

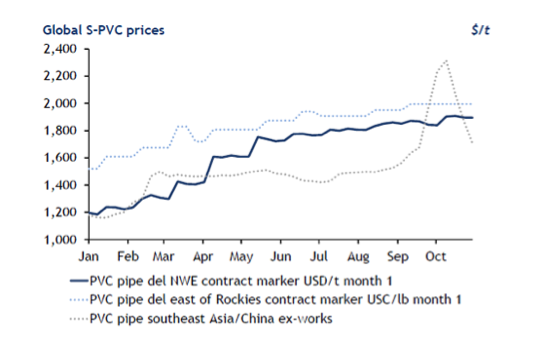

Case study 1: PVC price in 2021

Case study 2: US chemical product price

6.4 Financial Returns

Case study 1: US Chemical financial performance

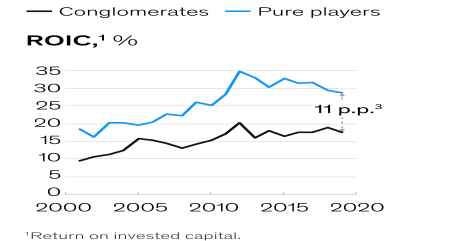

Case study 2: Return on Invested Capital

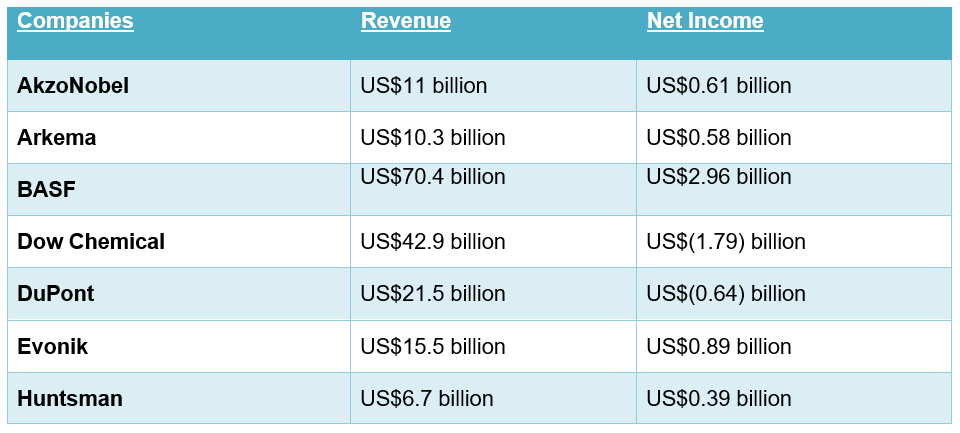

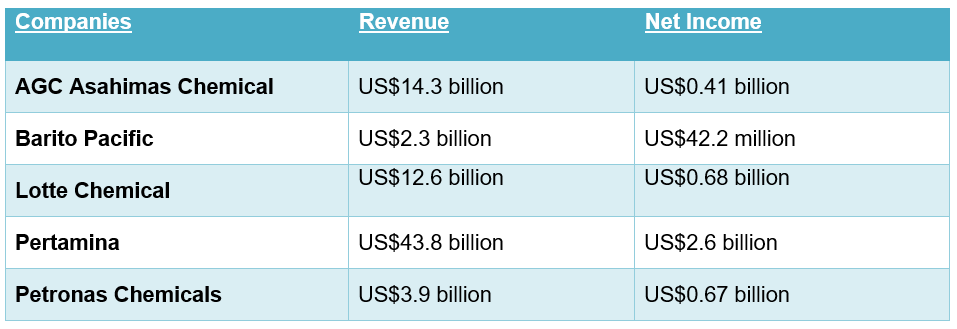

2019 Financial Income of listed international groups

Local Group: 2019 Financial incomes

6.5 Source of Funding

Funding for this venture can be sourced from various avenues, including:

1. Strategic Investors:

- New Investors: Business and financial management leaders interested in contributing to the project.

- Financiers: Specialty chemical private equity and investor groups that specialize in funding such ventures.

- Specialty Chemical Operators: International and local specialty chemical operator groups with a vested interest in the project.

- Target Market: Special chemical traders and licensed manufacturers from China, India, South East Asia, and Indochina who can provide investment support and market access.

2. Private Equities and Investors

- Abbrea Capital

- ADB (Asian Development Bank)

- Advent International

- AGC

- American Funds Global Balanced Fund

- Amundi Asset Management

- Apollo Global Management

- Ardian

- Bain Capital

- Baillie Gifford

- Banyan Tree

- Bencis Capital Partners

- Bernstein Fund

- BlackRock

- Blackstone

- Boston Partners Global Investors

- BPIFrance Investissement

- Bridge Builder International Equity

- Capital Income Builder

- Capital Research & Management

- Carlyle Group

- Cartica Capital

- CCLSA Capital

- Corporate Finance International

- Covéa Finance

- Credit Suisse

- Crescent Capital Consulting

- Deka Investment

- Dimensional Fund Advisors

- Dodge & Cox

- DWS Investments

- Eagle Global Advisors

- Eastspring Investments

- Edgepoint

- Elliott Investment Management

- Fidelity Management & Research

- First Horizon Advisors

- Flossbach von Storch

- Franklin Advisers

- Freedman Financial Associates

- Geode Capital Management

- GIC

- Harris Associates

- Henderson Global Investors

- Invesco Asset Management

- Jacob Ballas

- JANA Partners

- Kitara Capital

- KKR (Kohlberg Kravis Roberts & Co.)

- Lazard Asset Management

- Lester Murray Antman

- LSV Asset Management

- Macquarie

- Massachusetts Financial Services

- Meeder Asset Management

- Mitsubishi Corporation

- Mondrian Investment Partners

- Morgan Stanley Smith Barney

- Norges Bank Investment Management

- Northern Trust Investments

- Oman India Joint Investment Fund

- Private Capital Group

- Rabo Equity Advisors

- RAG-Stiftung

- Renaissance Group

- Samsung Asset Management

- Sands Capital Management

- Schroder

- Scopia Capital Management

- Scout Investments

- Sequoia Capital

- Sierra Capital

- Silvercrest Asset Management

- SK Capital

- Soroban Capital Partners

- SSgA Funds Management (State Street Global Advisors)

- Starboard Value

- Steward Partners Investment

- Templeton Global Advisors

- T. Rowe Price International

- Teachers Retirement System

- Thomas White International

- Thornburg Investment Management

- Todd Asset Management

- Union Investment Privatfonds

- Ursa Fund Management

- Vanguard Group

- VKB Portfolio Rendite Plus

- Wayzata Investment Partners

- William Blair

- Yacktman Asset Management

3. Consultants, Development, Procurement, and Fund Managers to the Specialty Chemicals Industry:

- American Chemistry Council (ACC)

- BCG (Boston Consulting Group)

- British Association for Chemical Specialties (BACS)

- Deloitte

- FCA (Food Contact Additives)

- Indian Specialty Chemical Manufacturers’ Association (ISCMA)

- Japan Chemicals Industry Association (JCIA)

- KPMG

- McKinsey & Co

- Motilal Oswal

- PwC (PricewaterhouseCoopers)

- Russian Chemists Union (RCU)

- Society of Chemical Manufacturers and Affiliates (SCOMA)

6.6 Where’s the Big Opportunity?

The significant opportunities for growth and success in the specialty chemical industry are:

- Volume Expansion: Leveraging established licensed manufacturers and distributors across Asia to capture a larger market share and increase production volume.

- Growth Through Acquisition: Accelerating growth by strategically acquiring complementary businesses and expanding the portfolio of specialty chemical products and services.

- Electric Vehicle Market: Capitalizing on the increasing demand for lithium hydroxide driven by the booming electric vehicle market, positioning the company as a key supplier in this rapidly growing sector.

7.0 Management Team

7.1 Key Management Team

- Mentors: Visionary pioneers and industry leaders with an extensive global network who provide invaluable guidance and inspiration.

- Coaches: Mission-oriented industry experts offering practical solutions to challenges, ensuring the team remains focused on its objectives.

- Partners:

- A project leadership group with a proven track record in the development, operation, and financial management of the specialty chemical industry.

- A reputable investment manager with access to funding sources within the specialty chemical industry.

- A respected local specialty chemical developer with strong procurement capabilities, a local network, sound financial stability, and solid government support.

- Target market end-users, importers, and licensed manufacturers.

In the specialty chemical industry, several global leaders have made significant contributions, shaping its growth and success. Here is a list of some of these remarkable individuals, honoured for their vision and dedication:

- Sir Leonard Valentinovich Blavatnik

- Martin Brudermüller

- Sergio Iorio

- Ren Jianxin

- Harish Kanani

- Sir James Arthur Ratcliffe

These are just a few of the outstanding professionals and captains of the industry. The readers are encouraged to explore further and conduct their research to learn more about the management teams in this dynamic field.

7.2 Key Management Team Model

8.0 Unique Business Model

8.1 Successful Track Record

- Proven success with branded products in niche segments.

- Consistent financial returns to investors.

- Advanced R&D and new product development, fostering customer loyalty and growth.

8.2 Entry Model

- Transforming the traditional specialty chemical industry through collaboration, acquisition, and mergers.

- Creating a unified entity in new markets.

- Partnering strategically with stakeholders across the value chain.

8.3 Unique Business Model

- Achieving cost efficiency through integration.

- Enhancing performance and financial returns through teamwork.

- Gaining direct access to domestic markets, serving as a springboard for Asia Pacific expansion.

9.0 Key Success Factors & Risk Mitigation

9.1 Key Success Factors

- Growth Potential: Leveraging a population of nearly 300 million in three nations for growth. Borneo’s manufacturing base serves as an ideal hub for the Asia Pacific region.

- Performance Standards: Setting performance benchmarks by collaborating with government departments to enhance competitiveness through technical features in national standards.

- Product Differentiation: Achieving product differentiation through continuous new product development.

- Strong Branding: Building a leadership brand, implementing customer loyalty programs, and offering incentives to attract and retain customers.

9.2 Risks

- Regulatory and Market Risks: Risks from regulatory changes, competition, supply and demand fluctuations, and technological disruptions.

- Commoditization: Potential for reduced margins and higher switching costs.

- Counterfeit Products: Risk of counterfeit and fake products damaging the brand image.

- Price Erosion: Intense competition among customers targeting the same markets leading to price erosion.

9.3 Risk Mitigation

- Government Support: Seek government support in drafting regulations to reduce regulatory risks.

- Enhanced Brand Image: Expand the distribution network, offer customized services, and provide technical and sales support to enhance product quality perception and stand out against low-cost alternatives.

- Education Programs: Conduct seminars, exhibitions, and marketing programs to educate buyers and combat counterfeit competitors. Engage licensed manufacturers in marketing efforts.

- Product Innovation: Invest in new product development with special formulations to differentiate products and expand the market.

- Capacity Building: Implement training programs for local teams in management, operations, processing, manufacturing, sales, and marketing to support market expansion.

10.0 Exit Strategy

10.1 Forms of Exit

- Potential exit options include IPO, buy-out, M&A, and asset transfer.

10.2 Key Attractions for New Investors

- Portfolio Diversity: Investment opportunities in emerging markets.

- Secure Demand: Partnerships with licensed manufacturers ensure stable demand.

- High Barriers to Entry: Significant initial investment costs create strong barriers.

- Cost Efficiency: Cost consolidation through new mergers and acquisitions.

- ESG Focus: Commitment to responsible corporate ESG practices aligns with purpose-driven investment.