“You are the light of the world. A city set on a hill cannot be hidden.”

Matthew 5:14 (ESV)

“I have never felt salvation in nature. I love cities above all.”

Michelangelo (1475-1564)

Discover the purpose of your work and your corporation

What is your purpose in work?

- You can improve the living standards of the people.

- You can Pioneer transformative initiatives on Borneo Island.

What drives your corporation’s core value?

- Identify this unique investment opportunity and capture greater market share.

- Make a positive impact in this developing economy and fostering job creation.

Indonesia New Capital–Nusantara

1.0 Executive Summary

Mission

- Form strategic alliances with a local government agency, an international infrastructure group, and a financial service provider for pioneering public-private partnership investments.

- Initiate Stage 1 with a US$27 billion investment in infrastructure and property development.

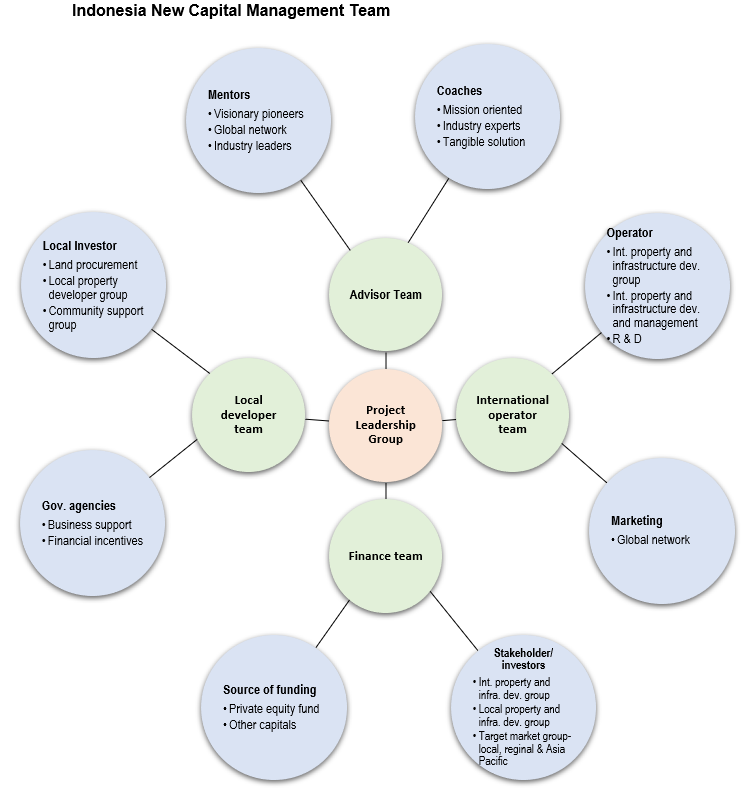

Key Management Team

- Mentors: Visionary pioneers and industry leaders offering invaluable guidance and inspiration.

- Coaches: Mission-oriented industry experts providing practical solutions to keep the team focused.

- Partners:

- Project Leadership Group: Proven success in city development.

- Investment Manager: Access to diverse funding sources.

- Government Agencies: Financial incentives and strong support.

- Local Developers: Procurement capabilities, local network, financial strength, government backing.

- Target Community: Support from the market community.

Product Benefits:

- Economic Boost: The new Borneo capital can become a focal point for Indonesia, Malaysia, and Brunei, with a total population of 306 million.

- PPP Advantages: Public-private partnership enhances flexibility and diversity in property and infrastructure projects.

- Hub Potential: Borneo poised to become the economic hub of the Asia Pacific, with a population of 4.6 billion and a GDP of US$31.58 trillion.

Target Market

- Segments: Property development and infrastructure projects

Financial Projections:

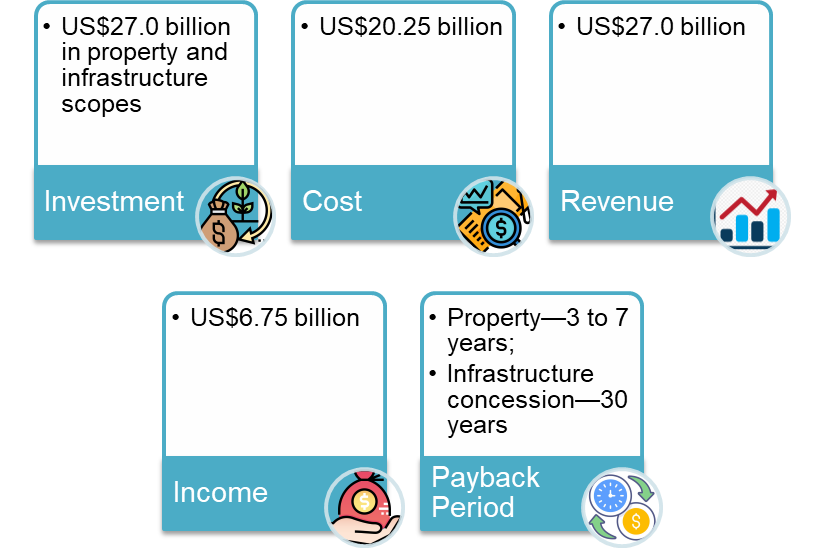

- Investment: US$27.0 billion in property and infrastructure scopes.

- Cost: US$20.25 billion.

- Revenue: US$27.0 billion.

- Income: US$6.75 billion.

- Payback: Property—3 to 7 years; Infrastructure concession—30 years.

Unique Business Model:

- Team Excellence: Assemble a top international management team with proven success.

- Strategic Partnerships: Combine strengths of stakeholders and investors in a unified entity.

- Financial Fortitude: Ensure a solid financial backing.

- Demand Assurance: Forge strategic partnerships with target customers to secure demand.

- Prime Location: Enjoy direct access to Asia Pacific markets.

2.0 Mission

2.1 Problem

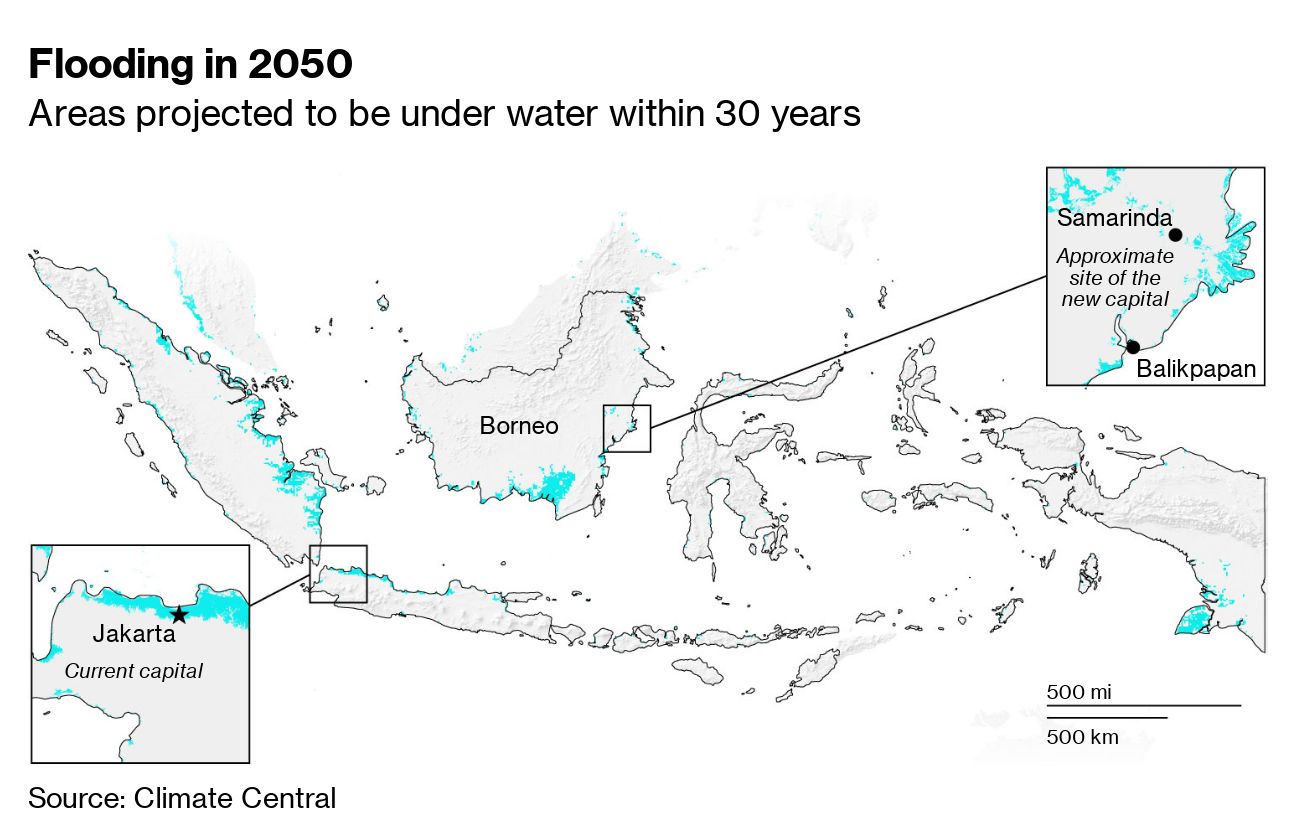

- Jakarta’s Challenge: Indonesia’s current capital, Jakarta, grapples with environmental and physical sustainability issues. What opportunities and challenges await investors?

2.2 Solution

- Strategic Site: The new capital, named Nusantara (meaning archipelago in Indonesian), will find its home on Borneo Island.

Indonesia New Capital in East Kalimantan (Borneo Island)

2.3 Mission

- Strategic Alliance Entity: Form a powerful coalition with a local government agency, international infrastructure group, and financial service provider to drive public-private partnership investments.

- Stage 1 Investment: Initiate a groundbreaking phase with a US$27 billion investment dedicated to infrastructure and property development.

3.0 Product

3.1 Product Description

- Location: Situated in East Kalimantan (Borneo) between Balikpapan and Samarinda.

- Area: Encompassing 256,142 hectares, including a government zone of 6,596 hectares and an IKN Area of 56,180 hectares. The IKN Development Zone spans 199,962 hectares, housing facilities for health, education, museums, technology parks, and more.

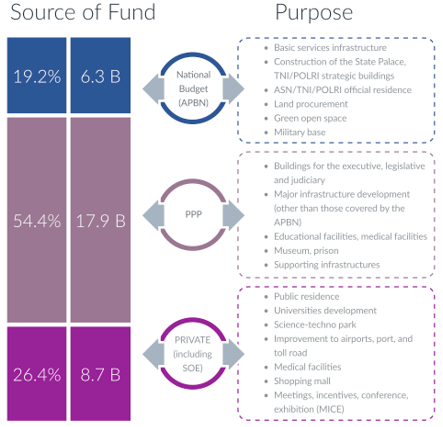

- Funding: The estimated cost for the new capital is US$33 billion, with 20% sourced from the Indonesian State Budget and 80% from private sector and PPP financing.

- Relocation: A significant step as 1.5 million civil servants embark on the relocation journey starting in 2024.

3.2 Product Attributes

- Risk: Minimal exposure to natural disasters.

- Economic Shift: Relocate economic activities to Kalimantan.

- Investment Model:

- Government Offices: US$6.3 billion (National Budget)

- Infrastructure, Schools, and Hospitals: US$17.9 billion (PPP)

- Residential and Commercial Property: US$8.7 billion (Private)

- Development Model: Private and PPP investment.

3.3 Product Benefits

- Economic Impact: The new Borneo capital can become the economic nucleus for Indonesia, Malaysia, and Brunei, with a combined population of 306 million—slightly larger than the USA.

- PPP Advantages: Public-private partnership enhances flexibility and diversity, fostering efficient implementation of infrastructure projects.

- Hub Potential: Positioned for regional economic prominence, Borneo aspires to be the hub for economic activities within the Asia Pacific, boasting direct access to a population of 4.6 billion and a combined GDP of US$31.58 trillion.

3.4 Product Competitive Advantages

- Speedy Progress:

- Private partnerships accelerate project development.

- Effective Team Collaboration:

- Strong government support aligns with well-established private sectors, tapping into a robust financial network.

- Guaranteed Returns:

- Government’s significant stake ensures a secure financial return.

4.0 Market

4.1 Market Segment

Investment segments: PPP and private segments

This image was first published in Ashurst’s Infraread – “Indonesia moves capital city: an illusion or an era of new opportunities?” on 19 November 2019 on www.ashurst.com Frederic Draps.

4.2 Target Market Strategy

The target market strategy will strategically unfold across Phase 2 and Phase 3.

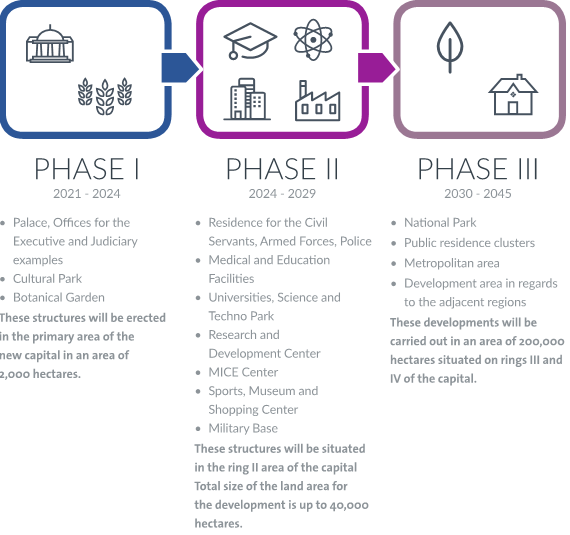

- Phase 1:

- Central Government Buildings

- Armed Forces and Police Quarters

- Diplomatic Sector

- Education Facilities

- Infrastructure (Roadwork, Power Generation, Telecommunication, Water Treatment, Waste Management, and Building Programs for the first 1-4 years)

- Phase 2:

- Residential and Commercial Development

- Universities

- Airport and Port

- MICE Building (Meetings, Incentives, Conferences, and Exhibitions)

- High-tech Park

- Phase 3:

- National Park

- Recreation and Arts Centre

- Further Residential and Commercial Development

Phase Development Graphics

This image was first published in Ashurst’s Infraread – “Indonesia moves capital city: an illusion or an era of new opportunities?” on 19 November 2019 on www.ashurst.com Frederic Draps.

4.3 Market Needs

The estimated cost of approximately US$33 billion will be met through a facilitated 20% from the government, with the private sector contributing the remaining 80%.

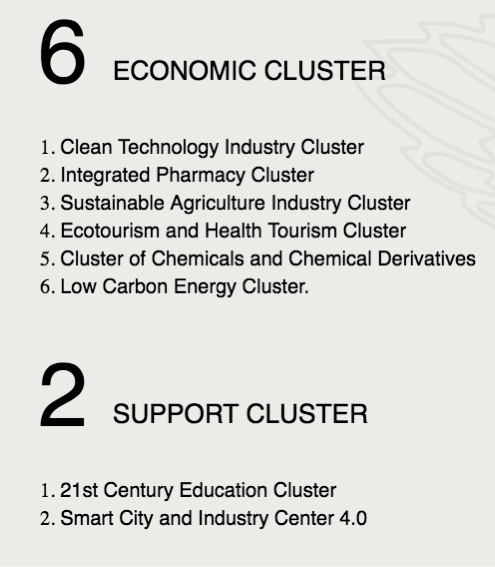

4.4 Growth Drivers

- Relocation of New Capital: The shift to the new capital serves as a catalyst for growth.

- Urban Migration: Increasing migration from rural to urban living propels market expansion.

- Economic Hub Investments: New economic and business ventures in the six economic hubs drive sustained growth.

4.5 Key Customers

Key stakeholders

- Indonesian Investment Authority (INA)

- Ministry of Agrarian and Spatial Planning / Head of the National Land Agency (BPN)

- Ministry of Finance

- Ministry of Forestry and Environmental Affairs

- Ministry of National Development Planning (BAPPENAS)

- Ministry of Public Works and Housing

- National Capital Authority of Nusantara (Otorita Ibu Kota Negara Nusantara)

- President of the Republic of Indonesia

4.6 Competition and Industry

Global infrastructure group

- Actividades de Construcción y Servicios

- Balfour Beatty

- Bechtel

- Bouygues

- China Communications Construction Company

- China State Construction Engineering Corp

- Hochtief Aktiengesellschaft

- Hyundai Engineering and Construction

- Kajima Corporation

- Kiewit Corporation

- Laing O’Rourke

- Larsen and Toubro

- Power China

- Skanska AB

- Strabag

- Technip FMC

- Turner Construction

- Vinci

- Whiting-Turner

Local property developers

- Agung Podomoro Land

- Agung Sedayu Group

- Ciputra Group

- Duta Anggada Realty

- Lippo Group

- Pakuwon Jati

- Permata Birama Sakti

- PP Properti

- RDTX Group

- Sinas Mas Land

- Tokyu Land Indonesia

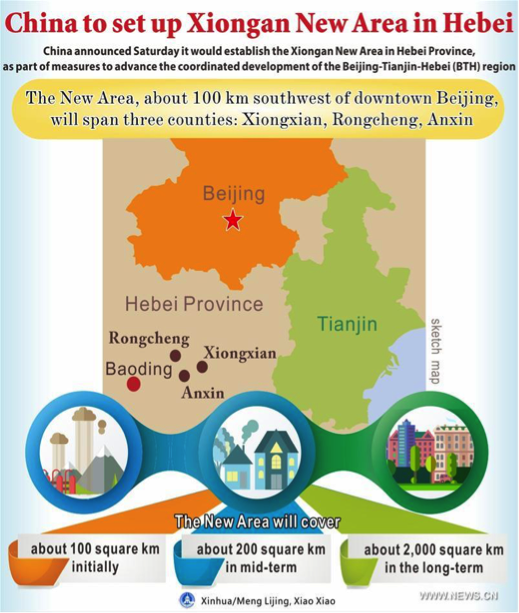

Recent new cities

Shenzhen population in million Xiong'an Initial 100 km² / Mid term 1990 = 2.7 M / 2020 = 17.6 M 200 km² / Long term 2000 km²

5.0 Operation

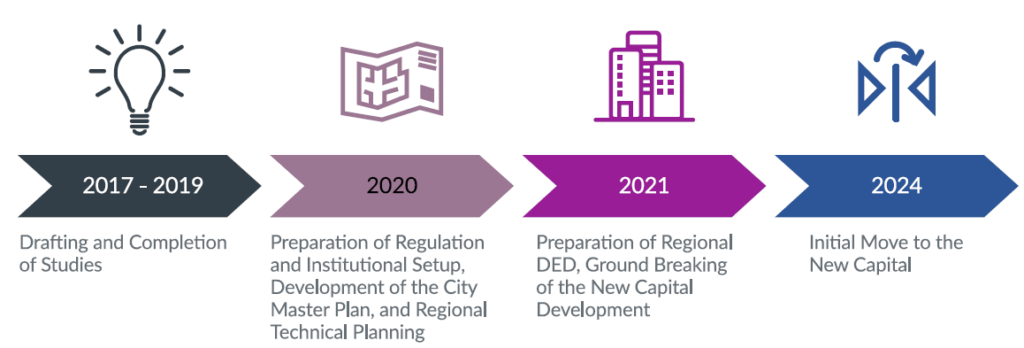

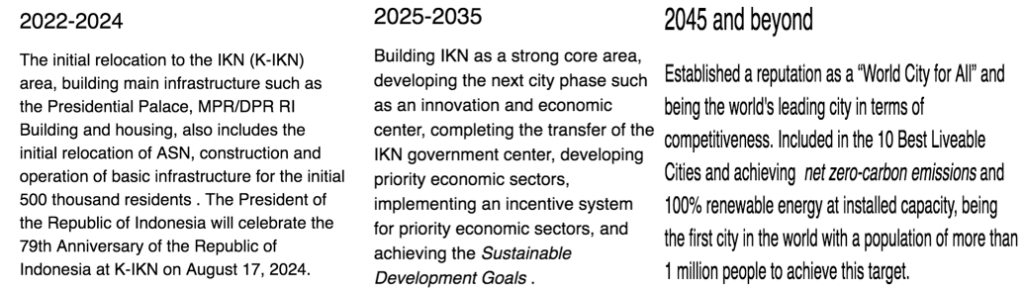

5.1 Estimated timeline for the new capital relocation

This image was first published in Ashurst’s Infraread – “Indonesia moves capital city: an illusion or an era of new opportunities?” on 19 November 2019 on www.ashurst.com Frederic Draps.

5.2 Scope

5.3 Development stages

6.0 Financial Implications

6.1 Investment Segment

Infrastructure Segment:

- Electricity

- Water

- Toll Roads

- Waste Management

- Telecommunications

- Transportation

- Port

- Airport

- Highways

- Other Services and Utilities

Land and Property Segment:

- In China, land sales constituted over 70% of the municipal government’s budget.

- Property values surged between 10-20 times over 30 years.

- Land values increased between 10-40 times over the same period, bolstering city and provincial government investments in infrastructure services.

Costs and Benefits

- The lesson learned from emerging markets heavily reliant on real estate development for funding new cities is the significant social and cultural impact on residents.

- The lower-income group, without transportation and housing subsidies, is particularly affected.

- There’s a crucial need for a balance between property prices and sustainable development to avoid negative impacts.

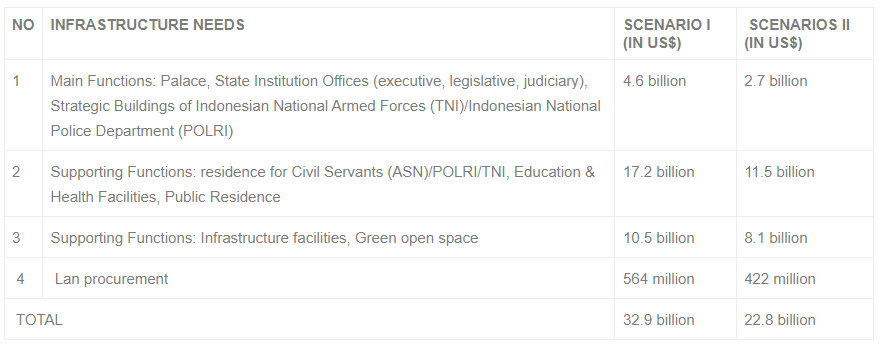

Indonesia’s new capital investment cost

This image was first published in Ashurst’s Infraread – “Indonesia moves capital city: an illusion or an era of new opportunities?” on 19 November 2019 on www.ashurst.com Frederic Draps.

Indonesia’s New Capital Investment Overview:

- Preliminary Budget: US$33 billion

- Initial Population: 3 million (projected to reach 6 million by 2050)

- Price: US$11,000 per resident

PPP and Private Sector Investment Scope:

- Investment of US$27 billion targeted for public-private partnership (PPP) and private sector involvement.

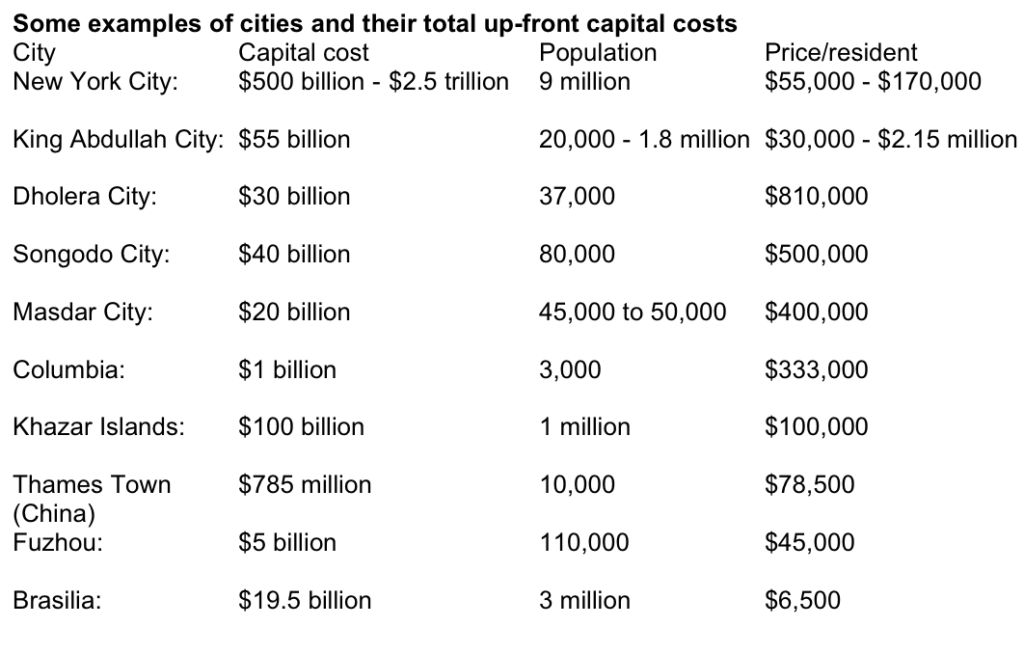

Case Study 1: CapitalFrontiers

- Cost Variation:

- Costs are contingent on on-site location and associated improvement conditions.

- New city development ranges from US$100,000 to US$1 million per resident.

- Population Impact:

- The cost is anticipated to decrease with the growth of the population.

6.2 Production Cost

Projected cost: US$27 billion X 75% = US$20.25 billion

6.3 Price and Revenue

International reference: 20–25% return Projected revenue: US$27 billion X 25% = US$6.75 billion

Case Study 1: Indonesia GDP per Capita 2019

- Jakarta: US$19,999

- Balikpapan: US$11,000

- Samarinda: US$5,560

- Projected GDP per Capita (2050): US$20,000 per person per year

Case Study 2: US GDP

- US GDP: US$75,000 per person per year

6.4 Financial Returns

1. Infrastructure Segment

Private fund and institutional investors seek a straightforward revenue pathway. The financial return model can be structured around:

- User Fees/Charges

- Capture Indirect Value: Generate revenue by selling indirect value.

- Financing Model Payments: Structured on agreed amounts, covering expenditure and ensuring returns.

- Asset Recycling: Strategically repurpose and recycle assets for sustained financial returns.

Case Study: Infrastructure Projects in Indonesia

Case 1: East Kalimantan Balikpapan–Samarinda 99 km Toll Road

- Estimated Project Cost: US$767 million

- FIRR (Financial Internal Rate of Return): 13.78%

- NPV (Net Present Value): US$260 million

- Estimated Concession Period: 40 Years

Case 2: Central Java Power Plant 2 X 1000 MW

- Estimated Project Cost: US$4,200 million

- FIRR: 11.12%

- NPV: US$938 million

- Estimated Concession Period: 25 Years

Case 3: East Java Umbulan Water Supply 4,000 lps

- Estimated Project Cost: US$140.7 million

- FIRR: 14.00%

- NPV: US$34.2 million

- Estimated Concession Period: 25 Years

Case 4: Sumatera and West Kalimantan Palapa Ring West Package (Fibre Optic 2,275 km)

- Estimated Project Cost: US$87.6 million

- IRR (Internal Rate of Return): 15.08%

- NPV: US$8.6 million

- Estimated Concession Period: 15 Years

Case 5: West Java Nambo Regional Waste Management 1500–1800 tons Waste/Day

- Estimated Project Cost: US$44.4 million

- FIRR: 13.60%

- NPV: US$4.8 million

- Estimated Concession Period: 25 Years

2. Property Segment

Developer:

- Target Market: Focus on the lower end of the housing market with strong demand.

- Affordability: Houses priced between US$35K and 40K, offering both affordability and a profitable financial return.

- Developer’s Expectation IRR: Above 25%.

Fund:

- Financial Interest: Affordable housing schemes attract strong interest from global financial institutions.

- Expectation IRR: Above 25%, with a targeted payback period of 4–7 years.

6.5 Source of Funding:

1. Strategic Investors

- New Investor: Project leader with a focus on business and financial management.

- Financier: Private equity and investor groups specializing in infrastructure and property.

- Developers: Collaboration with both international and local infrastructure developers and operators.

- Target Market: Attraction of investment from Indonesia’s private and sovereign funds.

2. Private Equities and Investors

- Advent International

- AEW Global

- Alpha Investment Partners

- Angelo Gordon

- Apollo Global Management

- APG Asset Management

- Ares Management

- AREA Property Partners

- Asian Development Bank (ADB)

- Asian Infrastructure Investment Bank (AIIB)

- Bain Capital

- Baring Private Equity Asia

- Beacon Capital Partners

- Blackstone Group

- Bridge Investment Group

- Brookfield Asset Management

- CapitaLand

- Carlyle Group

- CBRE Investment Management

- Cerberus Capital Management

- China’s Belt and Road Initiative (BRI)

- CIM Group

- Crow Holdings

- CVC Capital Partners

- D&J China

- ESR

- Fortress Investment Group

- GAW Capital Partners

- Goldman Sachs

- Harrison Street Real Estate Capital

- Infrastructure Asia

- International Development Finance Corporation (IDFC)

- Keppel Capital

- KKR

- Japan’s Partnership for Quality Infrastructure (PQI)

- LaSalle Investment Management

- Lone Star Funds

- Lubert-Adler Partners

- Morgan Stanley

- Northwood Investors

- Oaktree Capital Management

- Orion Capital Managers

- PAG

- Partners Group

- Perella Weinberg Partners

- PGIM Real Estate

- PIMCO

- Prudential Real Estate Investors

- Public Investment Fund (PIF)

- Rockpoint Group

- Shorenstein Properties

- Softbank

- Starwood Capital Group

- TA Associates Realty

- Thoma Bravo

- Tishman Speyer

- TPG Capital

- Tristan Capital Partners

- Walton Street Capital

- Warburg Pincus

- Westbrook Partners

- World Bank

3. Consultants, development, procurement and fund managers to the new capital city:

- Ashurst

- Bambang Brodjonegoro

- Capital Authority Agency (Indonesia)

- Deloitte

- Indonesian Investment Authority (INA)

- McKinsey & Company

- Oentoeng Suria & Partners

6.6 Future Expansion

- Growth Focus: The influx of new investments in infrastructure, property, healthcare, education, industry, and business is poised to catalyse significant economic activities in Borneo and the broader Asia Pacific region.

7.0 Management Team

7.1 Key Management Team

- Mentors: Visionary pioneers and industry leaders offering invaluable guidance and inspiration.

- Coaches: Mission-oriented industry experts providing practical solutions to keep the team focused.

- Partners:

- Project Leadership Group: Proven success in city development.

- Investment Manager: Access to diverse funding sources.

- Government Agencies: Financial incentives and strong support.

- Local Developers: Procurement capabilities, local network, financial strength, government backing.

- Target Community: Support from the market community.

In the new city development industry, several global leaders have made significant contributions, shaping its growth and success. Here is a list of some of these remarkable individuals, honoured for their vision and dedication:

These are just a few of the outstanding leaders, professionals and captains of the industry. The readers are encouraged to explore further and conduct their research to learn more about the management teams in this dynamic field.

7.2 Key Management Team Model

8.0 Unique Business Model

8.1 Successful Track Record

- Team Composition: The team is a blend of international and local property developers, infrastructure operators, financial service providers, investors, and supportive government agencies, all boasting successful track records.

8.2 Entry Model

- Private: The private sector assumes the entire development scope.

- PPP (Public-Private Partnership): Collaboration in PPP investments between government agencies and the private sector.

8.3 Unique Business Model

- Team Expertise: A specialized team with a proven track record in performance, productivity, and financial returns.

- Branding Impact: International network exposure facilitating access to funding, technology, and management.

- Strategic Location: Direct access to the Asia Pacific markets.

- Demand Assurance: Securing demand through strategic alliances with end-user groups.

9.0 Key Success Factors & Risk Mitigation

9.1 Key Success Factors

- Policy: Strong central and local government policies.

- Facilities: Robust infrastructure facilities, including utilities, transport, healthcare, and education.

- Living: Emphasis on quality living, parks, and cultural aspects.

- Team: Collaboration of government agency initiatives, financial resources, private investors, and international developers and operators with a global network.

- Economic: Business and manufacturing investments generating jobs and economic growth.

- Unity: The new capital’s potential to define national identity and foster unity, instilling pride among citizens.

9.2 Risks

- Return: Bankability challenges in attracting reputable financial service providers. The need to identify and address bankability performance in infrastructure projects for funding the new capital. Government agencies and fund managers must meet acceptable risk profile criteria.

- Clarity: Ensuring a clear vision in tangible terms to make stakeholders aware of the cost and benefits of the scope.

9.3 Risk Mitigation

- ESG (Environmental, Social, Governance): Professional consultants and independent auditors ensuring significant corporate governance, evaluating projects’ feasibility, profitability, and environmental and social impact.

- Mitigation: Collaborative risk mitigation efforts among consenting partners to reduce infrastructure risks, including political, macroeconomic, business, and technical risks.

- Policy: Government-led mitigation of risks associated with tariffs, regulations, policies, and land acquisition.

- Shared Responsibility: The private sector sharing risks in finance, construction, operational management, and associated costs in these segments.

10.0 Exit Strategy

10.1 Forms of Exit

- Forms: IPO, buy-out, M&A, and transfer.

10.2 Key Attractions for New Investors

- Capacity: New investors continue as operators of infrastructure and property projects.

- Portfolio: Projects in the new capital offer alternative investments in an emerging market.

- Demand: Partnership with government and end-users ensures secured demand.

- Barrier: High barriers to entry due to substantial investment costs.

- Growth: Opportunities to capture growth in an emerging market.

- ESG: Responsible corporate practices with a purpose-driven investment approach.