“Even to prepare me timber in abundance: for the house which I am about to build shall be wonderful great.”

2 Chronicles 2:9 (KJV)

“We are consuming our forests three times faster than they are being reproduced. Some of the richest timberlands of this continent have already been destroyed, and not replaced, and other vast areas are on the verge of destruction. Yet forests, unlike mines, can be so handled as to yield the best results of use, without exhaustion, just like grain fields.”

President Theodore Roosevelt 1907

Discover the Purpose of Your Work and your Corporation

Understanding the deeper purpose behind your work and the mission of your corporation is vital. In the context of the timber industry, it becomes especially poignant as we consider the environmental impact and the potential for positive change.

Your Purpose in Work: Making a Difference in Borneo Island

One of the most profound purposes in your work is the ability to make a significant difference in Borneo Island. The rampant illegal and unsustainable logging in this region has wreaked havoc on the environment. It has destroyed precious wildlife habitats, led to soil degradation, caused devastating flooding, and inflicted suffering on the inhabitants. By engaging in this industry responsibly, you have the power to halt these destructive practices, preserving the natural beauty of Borneo and safeguarding its people and wildlife.

Contributing to Positive Environmental Impact: Investing in Timber Plantation

Another crucial facet of your work is the opportunity to contribute to a positive environmental impact. By investing in timber plantations, you are not only ensuring a sustainable supply of timber but also actively participating in the restoration of natural habitats. This investment serves as a beacon of hope for the environment, helping it recover from years of abuse.

What Drives Your Corporation’s Core Values: Capturing Urgent Needs and Leading the Industry

Your corporation’s core values are deeply intertwined with its mission. It revolves around identifying a unique opportunity and addressing the urgent need for sawn timber in Asia. In doing so, you take on the role of an industry pioneer, initiating a tropical reforestation program in Borneo. This leadership position is not only a testament to your commitment but also a beacon for others in the industry to follow.

Continuing Blessings: Wildlife, Soil, Green Lungs, and Timber Demand

The purpose of your work and your corporation transcends mere profit. It is a noble endeavour that continues to bless the world in multifaceted ways. Through your dedication, you protect and restore wildlife habitats, prevent soil erosion, create new green lungs for our planet, and meet the immense demand for tropical timber, ensuring a sustainable future for generations to come.

Eucalypts Plantation

1.0 Executive Summary

Mission

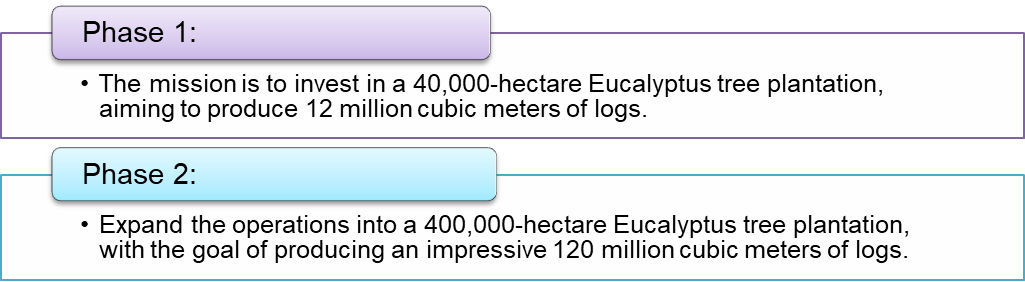

- Phase 1: The mission is to invest in a 40,000-hectare Eucalyptus tree plantation, aiming to produce 12 million cubic meters of logs.

- Phase 2: Expand the operations into a 400,000-hectare Eucalyptus tree plantation, with the goal of producing an impressive 120 million cubic meters of logs.

Key management team

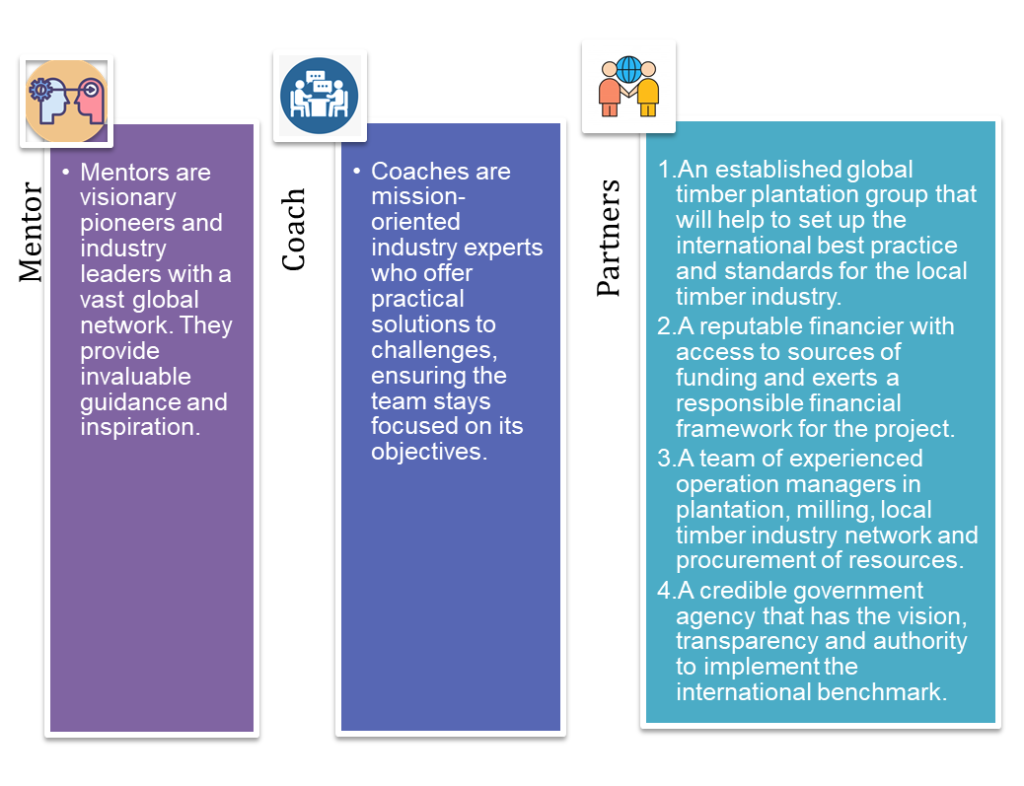

- Mentor:

Mentors are visionary pioneers and industry leaders with a vast global network. They provide invaluable guidance and inspiration.

- Coaches:

Coaches are mission-oriented industry experts who offer practical solutions to challenges, ensuring the team stays focused on its objectives.

- Partners:

1. An established global timber plantation group that will help to set up the international best practice and standards for the local timber industry.

2. A reputable financier with access to sources of funding and exerts a responsible financial framework for the project.

3. A team of experienced operation managers in plantation, milling, local timber industry network and procurement of resources.

4. A credible government agency that has the vision, transparency and authority to implement the international benchmark.

Product Benefits

- The planned plantation (silviculture) offers the advantage of providing a predictable supply at a known cost.

- Timber plantations can yield between 300-600 cubic meters per hectare of timber, a substantial improvement over the 60-150 cubic meters per hectare found in primary forests.

- The commitment to sustainable forest management ensures compliance with international certification, reducing the impact of logging and preserving wildlife habitats.

Target Market

- The Borneo timber plantation will effectively meet the urgent demand of local timber mills.

- Malaysia’s local timber mills require 30 million cubic meters of timber logs annually.

- Indonesia, a key market, demands 85 million cubic meters of timber logs each year.

Financial Projections

- Total investment: US$1.4 billion

- Production cost: US$11.4 billion

- Revenue: US$22.8 billion

- Income: US$11.4 billion

- Payback period: 25-year cycle rotation

Unique Business Model

- The unique business model revolves around a fully integrated commitment shared among stakeholders with aligned goals.

- Saw millers and end buyers of plantation logs benefit from specified timber quality, volume, and pricing structures.

- The producer operates within set parameters of quantity and cost structures.

- Private equity fund investors gain assurance in achieving business and financial expectations.

- The rapid market entry model involves the purchase or leasing of existing plantation concession land.

2.0 Mission

2.1 Problem

- At present, a significant timber log shortage plagues the sawn timber mill industries in Borneo, encompassing regions such as Sabah, Sarawak, and Kalimantan.

- The issue of illegal and unsustainable logging has left a devastating mark, resulting in the depletion of 70% of Borneo’s natural forests over recent decades. This rampant greed has not only destroyed critical wildlife habitats but has also led to soil degradation, flooding, and immense suffering for the local inhabitants. Tragically, the last Bornean rhinoceros in Sabah perished in 2019, marking the official extinction of this species in Malaysia.

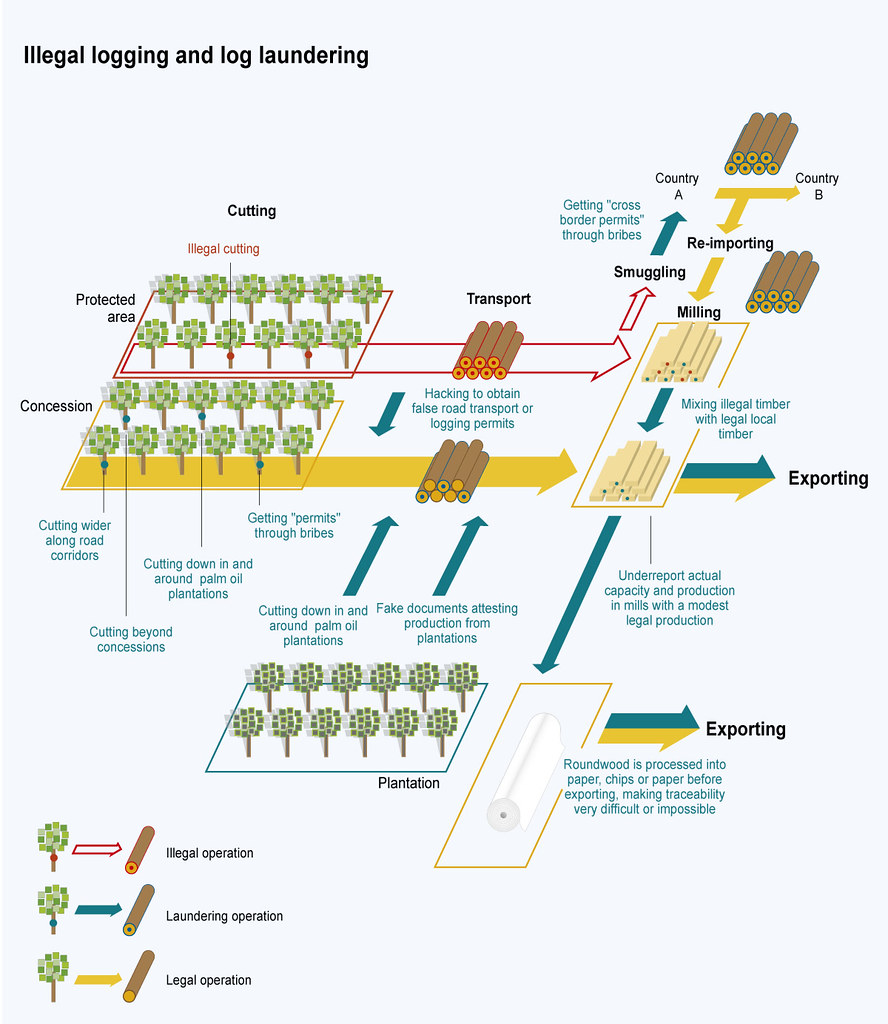

Illegal logging and log laundering

Illegal logging has destroyed about 10 million hectares of Indonesian forest and deforested millions of hectares in Borneo Island.

2.2 Solution

- Establish a strategic alliance with a local government agency, an internationally reputable timber company, and a responsible financial service provider.

- Investments in timber plantation development, catering to both domestic and export markets.

- Borneo, with its expansive land availability, emerges as the optimal location for reforestation, simultaneously safeguarding sustainable habitats for wildlife.

- Commitment to mandating sustainable timber production and trade, adhering to globally recognized certifications such as FSC (The Forest Stewardship Council) and Sustainable Forest Management (SFM), among others.

2.3 Mission

- Phase 1: Invest in a 40,000-hectare Eucalyptus tree plantation, with the goal of producing 12 million cubic meters of logs.

- Phase 2: Expand to encompass a 400,000-hectare Eucalyptus tree plantation, aimed at yielding 120 million cubic meters of logs. This ambitious phase highlights the commitment to sustainable forestry practices and the restoration of Borneo’s ecosystem.

3.0 Product

3.1 Product Description

The product comprises high-quality logs harvested from Eucalyptus tree plantations. These logs serve a multitude of purposes, including but not limited to sawn timber, dry veneer, plywood, fuel pellets, poles, flooring, laminated veneer lumber, furniture, joinery, and various construction products. Blue Gum Eucalyptus is one of the most widely cultivated plantation trees worldwide.

3.2 Product Attributes

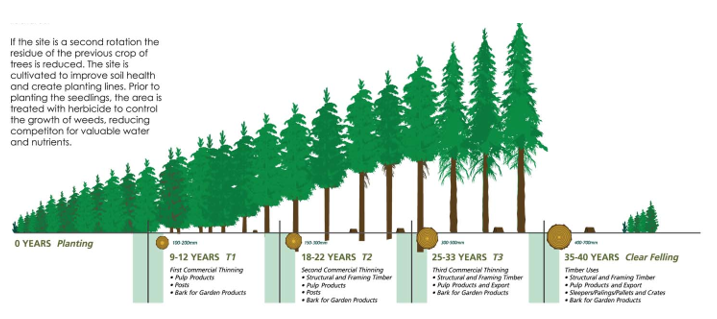

- Eucalyptus trees exhibit rapid growth compared to most hardwood species with similar wood density.

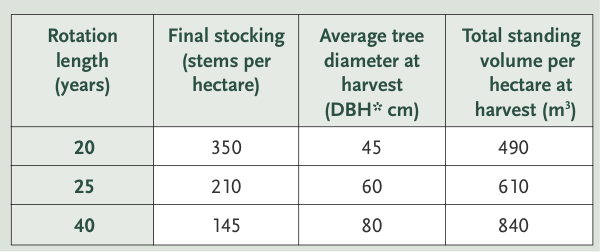

- The harvesting process includes the first commercial thinning at year 8, followed by a second thinning at year 18, culminating in the final clear felling at year 25.

- Eucalyptus timber is known for its durability, versatility, aesthetic appeal, biodegradability, and renewable nature.

3.3 Product Benefits

- The planned plantation model ensures a consistent supply of timber at a known cost, providing stability to our customers.

- Eucalyptus timber plantations yield significantly higher quantities, ranging from 300-600 cubic meters per hectare, in comparison to the 60-150 cubic meters per hectare typically obtained from primary forests.

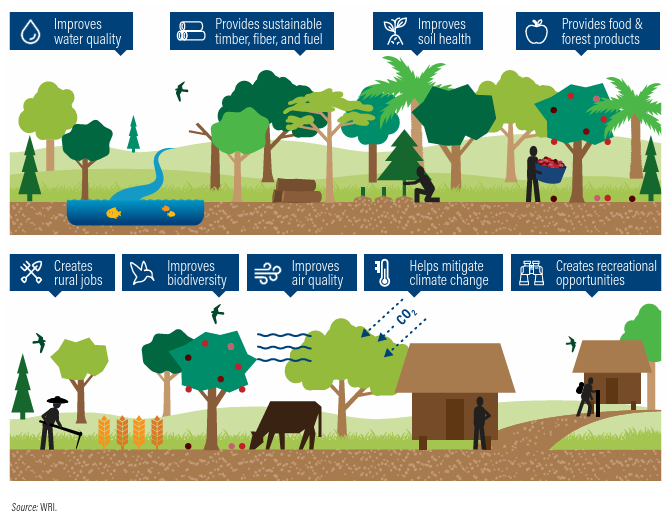

- The team must firmly commit to sustainable forest management practices that align with international certification standards, ensuring responsible timber production and enhance the success of wildlife protection.

Benefits of timber plantation

3.4 Product Competitive Advantages

- The initiative actively reduces land degradation and combats illegal logging on idle forestry land. Previously logged natural forest areas receive vital forest restoration. Borneo’s governments actively endorse and support reforestation programs for sustainable forest management.

- Borneo’s strategic location provides a competitive edge with cost-effective land access options and proximity to the Asia Pacific market. The tropical climate, characterized by abundant sunshine and rainfall, promotes a higher timber yield. This unique geographical positioning grants direct access to the lucrative Asian market.

- The timber plantation fosters alignment with international stakeholders, enhances the image of governments involved, garners positive global exposure, and strengthens wildlife protection efforts. This synergy of interests contributes to the success and sustainability of our endeavour, benefiting not only the business but also the environment and local communities.

4.0 Market

4.1 Market Segments

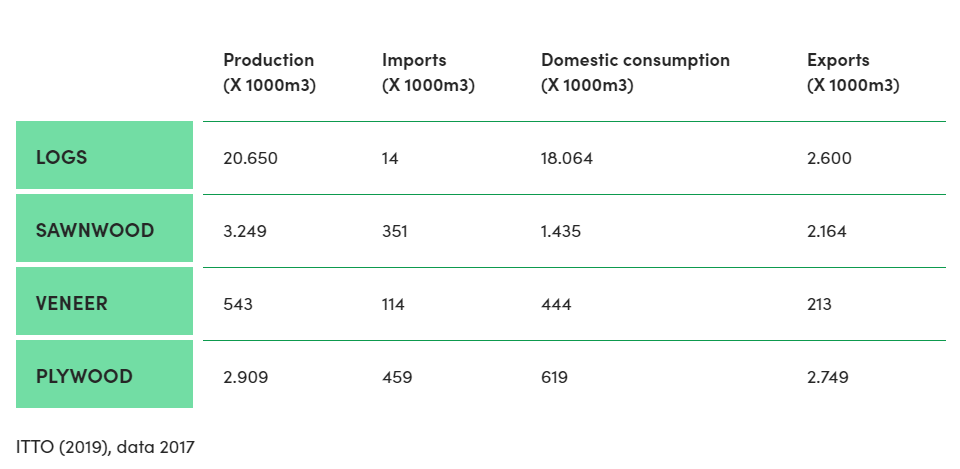

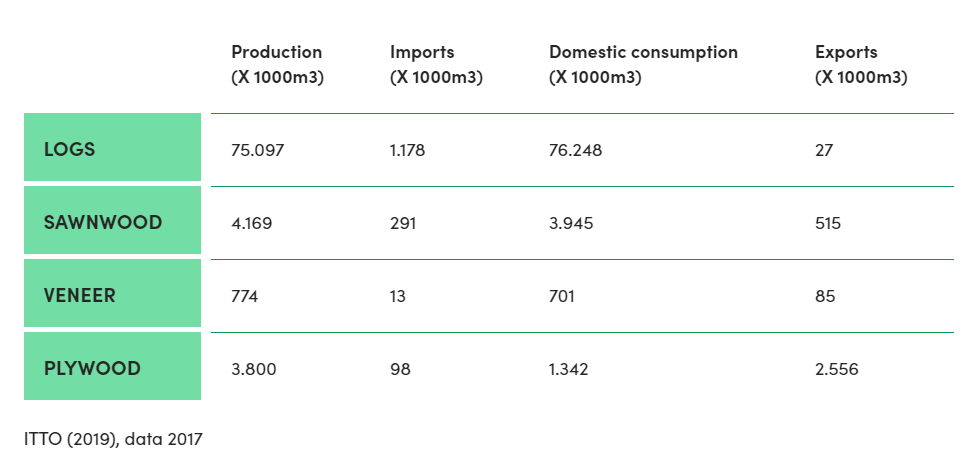

Forested land in Malaysia (2017):

- Sarawak: 8.03 million hectares

- Peninsular Malaysia: 5.80 million hectares

- Sabah: 4.44 million hectares

- Total: 18.27 million hectares

Forested land in Indonesia (2017):

- Primary forest: 86.1 million hectares

- Planted forest: 4.9 million hectares

- Total: 91 million hectares

Kalimantan:

- 11 million hectares of protected forest

Brunei:

- Forested land covers 0.527 million hectares, with 70% as primary forest and 30% as other wooded areas.

The two primary sources of timber supply are:

1. Natural timber, found in Permanent Reserved Forests:

- Sarawak: 4.9 million hectares

- Peninsular Malaysia: 4.8 million hectares

- Sabah: 3.54 million hectares

- Total: 13.24 million hectares Note: Logging activities are generally restricted in these areas.

2. Timber plantations in Borneo:

- Sarawak: 420,000 hectares

- Sabah: 158,000 hectares

- Kalimantan: Borneo Initiative has a 10-year program plan for 4 million hectares of reforestation in Kalimantan.

4.2 Target Market Strategy

Malaysia is home to over 4,000 timber mills engaged in processing furniture, sawmills, mouldings, plywood, veneer, wood chips, kiln drying, builders joinery carpentry, and medium-density fibreboard.

- A green sawmill processing facility requires an annual timber log supply of 30,000 cubic meters.

- Sawmills processing air or kiln-dried timber (dry mills) demand approximately 50,000 cubic meters of timber logs per year.

- Dry veneer plywood mills require an annual supply of 50,000 cubic meters.

- Structural plywood mills serving the construction industry need 100,000 cubic meters of logs annually.

Sabah has banned the export of logs, while Sarawak maintains strict quotas for Forest Timber Licenses. Similarly, Indonesia discourages the export of timber logs. As a result, timber sawmills in Borneo are increasingly dependent on timber plantations to meet their needs.

4.3 Market Needs

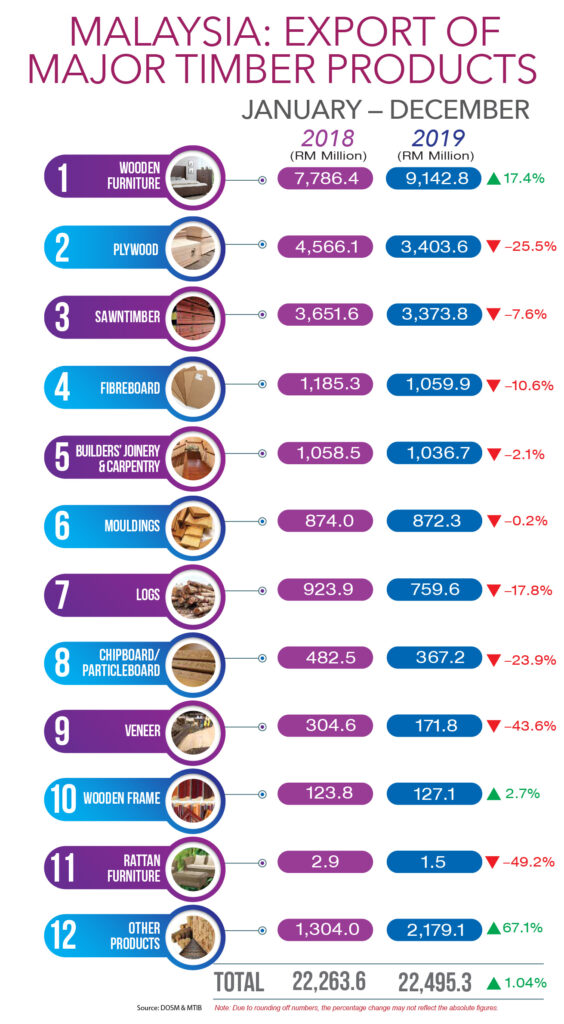

Malaysia’s export of timber products has shown substantial value:

- 2018: US$5.357 billion

- 2019: US$5.413 billion

These timber products are often exported as finished goods to developed countries, with India and China being the largest importers of tropical hardwoods, accounting for 80% of global imports.

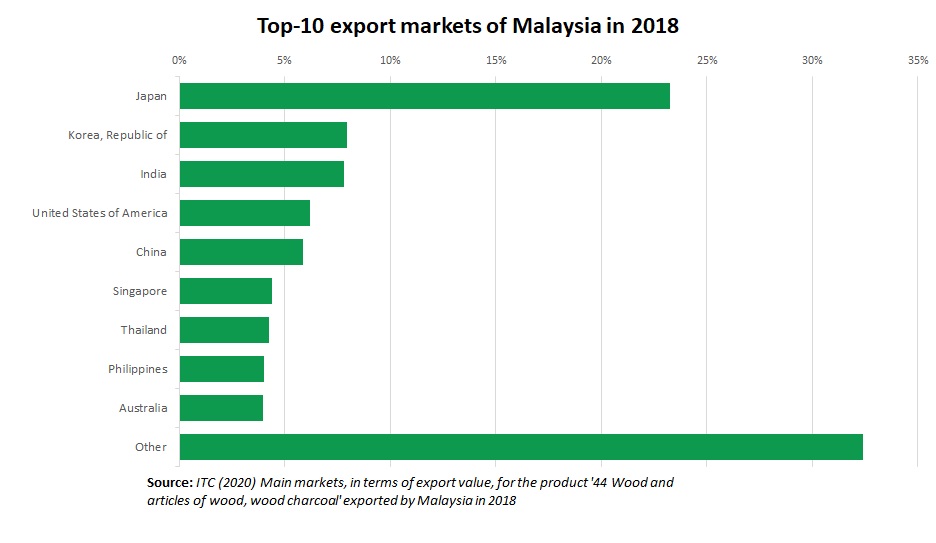

Malaysia timber major export market

Indonesia timber major export market

Malaysia timber market demand

Sabah and Sarawak collectively need to produce 30 million cubic meters of logs annually to meet the demands of local timber mills. This equates to 100,000 hectares of timber plantation each year. To satisfy this demand over a 25-year rotation cycle, 3 million hectares of plantation are needed, but only 20% of plantations have met this goal to date. This leaves a substantial requirement for an additional 2.4 million hectares.

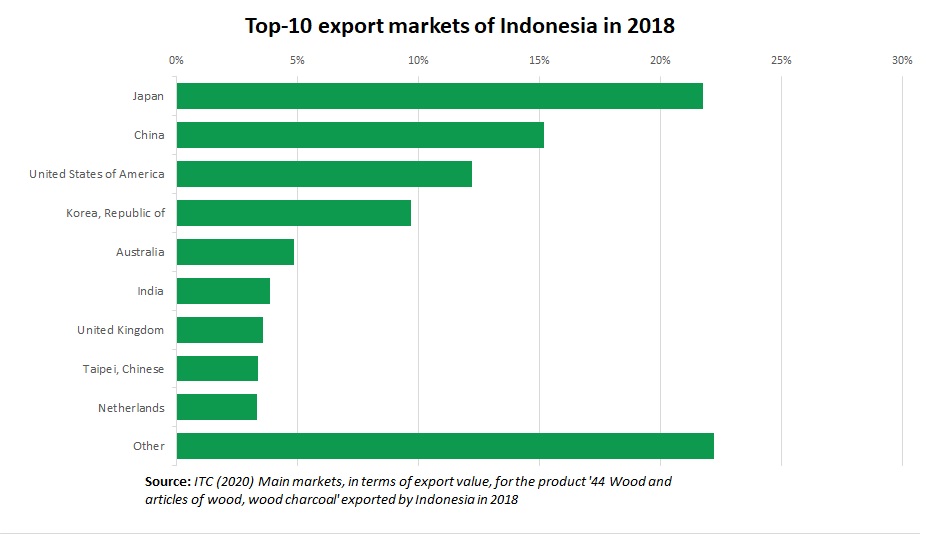

Indonesia timber major export market

In Kalimantan, the need is even more significant, requiring 85 million cubic meters of logs annually. This translates to 285,000 hectares of timber plantation per year, or 7.2 million hectares over a 25-year rotation cycle. Currently, only 4 million hectares of timber plantation meet this target, necessitating an additional 3.2 million hectares.

- Sarawak requires an additional 2 million hectares of timber plantation.

- Sabah needs an extra 0.4 million hectares of timber plantation.

- Kalimantan requires another 3.2 million hectares of timber plantation.

4.4 Growth Drivers

- Malaysia sees 17% of its timber products headed for the US market and 18% to Japan.

- In 2018, Indonesia exported US$3.7 billion worth of timber, furniture, and other finished wood products to China, accounting for 28% of its total exports in this category.

Growth drivers include:

- Rising demand for sawn timber in the construction and furniture sectors, both locally and for export.

- China is expected to face an annual wood deficit of 200 million cubic meters by 2025, creating a substantial market opportunity.

4.5 Key Customers

Sawmills in Borneo, segmented by region:

- Brunei sawmills: 20

- Sabah sawmills: 76

- Sarawak sawmills: 67

- Kalimantan sawmills: 161

4.6 Competition and Industry

- Reforestation:

- Most reforestation plantations primarily supply the pulp and paper industries, focusing on short-term returns. The model for sawn timber production typically involves long-term investments, making it less attractive to the local industry.

- Yield:

- A well-managed plantation growing at a Mean Annual Increment (MAI) of 12-24 cubic meters per hectare per year over a 25-year rotation will yield approximately 300-600 cubic meters per hectare. This is a significant improvement over the 60-150 cubic meters per hectare found in natural forests.

- Borneo’s timber plantations yield between 16-26 cubic meters per hectare per year.

- Land:

- Borneo Island stands out as an ideal location due to its vast available land for timber plantations. The island’s tropical climate is favorable for rapid forest growth, and governments endorse renewable timber plantation policies.

- Local Timber Plantation Companies:

- Most local plantation companies prioritize fast-growing softwood species for the downstream industry, offering quick returns. Few foreign-funded companies focus on hardwood species for their timber plantations.

The market analysis reveals significant opportunities for sustainable timber production and underscores the importance of the strategic initiative in addressing the region’s timber supply needs.

Local group

Acacia Forest Industries Adindo Hutani Lestari Alas Kusuma Group APP (Sinar Mas), APRIL Asia Pacific Resources Barito Pacific Group Bidasari, Bina Balantak Utama Borneo Hijau Lestari Bornion Timber Erna Djuliawati Harwood Timber Company Hijauan Bengkoka Plantations Hutan Ketapang Industri Indexim Utama (Surya Satrya Timur) Forest Solutions ITCI Hutani Manuggai Jawala, Kalimanis Group Kayu Lapis Group Komill Corporation Korondo Group Kutai Timber Group KTS Plantation Lamitech International Narkata Rimba Nusantara Fiber Pusaka, Rimbunan Hijau Group Roda Mas, Royal Golden Eagle Sabah Forest Industries Safoda Samling Group Sapulut Forest Development Sari Bumi Kusuma Shin Yang Group Subur Tiasa Holdings Suka Jaya Makmur Sumatera Dinamika Utama Ta Ann Group Telaga Bakti Persada Timberwell Titan Superindo Toba Pulp Lestari TSH Resources WTK Group

Organisation

ABARES (Australian Bureau of Agricultural and Resource Economics) Brunei Forestry Department Forest Area Planning & Management in Kalimantan (KALFOR) Indonesian Ministry of Environment and Forestry Malaysian Timber Council (MTC) Sabah Timber Industries Association STIA Sabah Forestry Development Authority (SAFODA) Sarawak Timber Association (STA) Sarawak Timber Industry Development Corporation (STIDC) The Forest Stewardship Council (FSC) Timber Association of Sabah (TAS) Tropical Forest Foundation (TFF) Yayasan Sabah, Yayasan IDH

5. Strong Competition for Land

- Land: There is a pressing demand for land conversion to oil palm cultivation. However, reforestation is an urgent necessity that warrants immediate attention. Local governments are likely to support this vital policy.

- Shortage: The shortage of log supply for downstream industries is severe. Consider this critical perspective: “There are two best times to plant a tree. The best time to plant a tree was 25 years ago. The second-best time is now.”

4.7 Borneo’s Competitive Advantages

- Land: Borneo’s strategic location is advantageous for agriculture, offering direct access to the Asia Pacific market.

- Yield: Eucalyptus plantations in Borneo boast an impressive yield of 16–26 cubic meters per hectare per year.

- Cost: Lower planting costs in Borneo make it an attractive destination for sustainable timber production.

- Demand: Borneo enjoys direct access to the local sawmill market, where there is a 100% demand for timber, underscoring its significant market advantage.

In light of these competitive advantages, Borneo emerges as a pivotal player in addressing the critical need for sustainable timber production, while also mitigating the challenges posed by land conversion pressures and log shortages in the region.

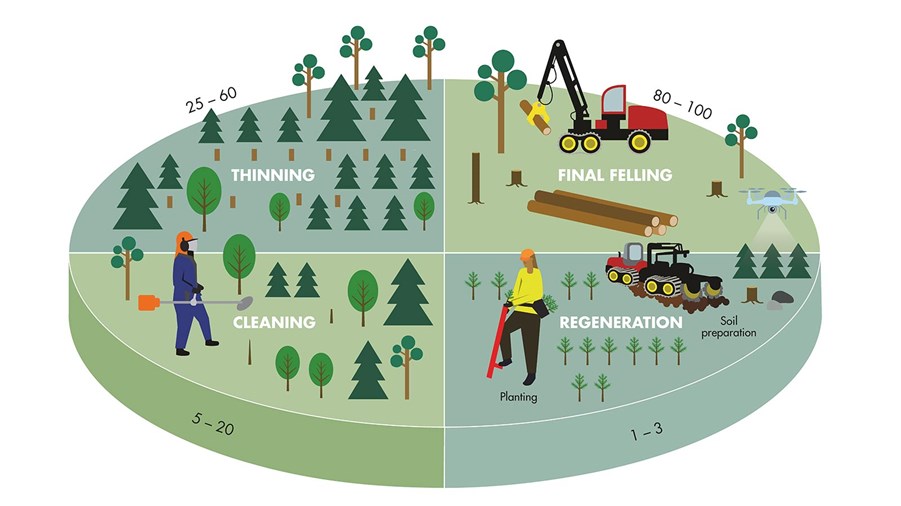

5.0 Operation

5.1 The cycle of forestry

5.2 Land

Key factors to consider in site selection:

- Suitable terrain and topography, soil conditions, pests and diseases management, quality of planting material.

5.3 Tree Nursery 5.4 Site establishments 5.5 Planting 1,500

tree/hectare

5.6 Tree Thinning at year 9, 18, and 25

5.7 Harvest at year 25

5.8 Yield

6.0 Financial Implications

6.1 Investment Segments

Timber plantation investment segments

Investment options:

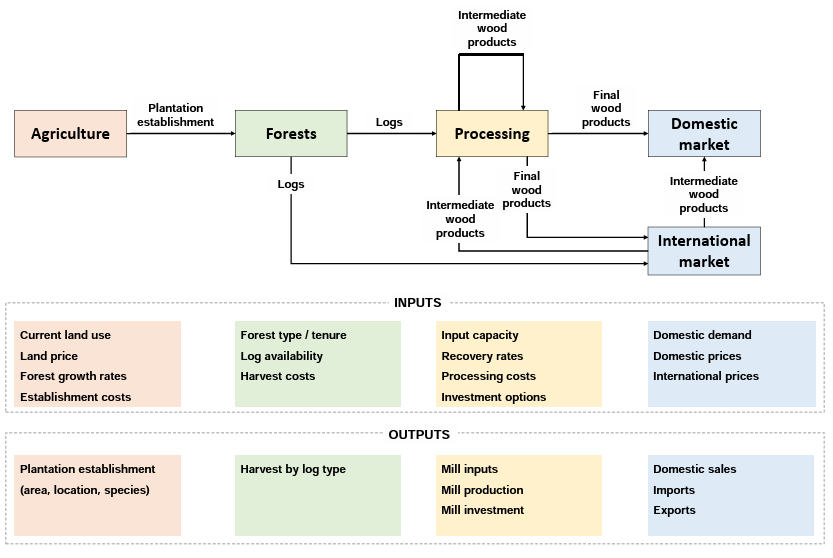

Investment in the timber industry can be categorized into three main segments:

- Upstream: Involves planting, cultivation, and harvest of timber.

- Midstream: Focuses on sawmills and processing of timber.

- Downstream: Encompasses the manufacturing of products such as furniture, veneer, construction materials, and engineering timber.

Investment Plan:

- In Sabah, 600,000 hectares of land have been allocated for timber plantation, with 400,000 hectares designated for tree planting.

- Currently, 160,000 hectares have been planted, leaving an opportunity to utilize an additional 240,000 hectares of land.

- Phase 1: The initial investment will concentrate on the upstream segment in Sabah, with a focus on establishing a 40,000-hectare Eucalyptus tree plantation. The estimated investment cost for this phase is approximately US$3,500 per hectare, requiring a total budget of US$140 million.

- The investment will expand to encompass 400,000 hectares across the rest of Borneo, including Brunei, Sarawak, and Kalimantan. The total investment budget for this expansion is projected to be US$1.4 billion.

- With an anticipated yield of 300 cubic meters per hectare, the total production of logs is expected to reach 120 million cubic meters.

- Upstream productions will include chips logs, sawn logs, and veneer logs.

- Future investment targets will include the midstream segment, focusing on wood chips, sawn timbers, and veneer, as well as the downstream segment, covering products like cross-laminated timber, glued laminated timber, laminated veneer lumber, furniture, construction timber, and building frames.

- In 2020, Forest Management Concession land in Sabah was sold for US$143.2 million, covering 235,000 hectares, amounting to approximately US$510 per hectare.

- The cost of cultivating trees in permitted logging spaces or plantations in 2019 ranged between US$1,500 per hectare and US$3,500 per hectare.

Summary of Investment:

- Total Investment for 400,000 hectares: US$1.4 billion

- Phase 1 Investment for 40,000 hectares: US$0.14 billion

6.2 Production Cost

Logging harvest cost ranges between US$63–$95/m3.

- Total Production Cost for 120 million cubic meters:

- 120 million m3 x $95/m3 = US$11.4 billion

- Phase 1 Production Cost for 12 million cubic meters:

- 12 million m3 x $95/m3 = US$1.14 billion

6.3 Prices and Revenues

The estimated income at harvest on a 25-year cycle rotation for Eucalyptus species is as follows:

- Total Estimated Income for 120 million cubic meters:

- 120 million m3 x $190/m3 = US$22.8 billion

- Phase 1 Estimated Income for 12 million cubic meters:

- 12 million m3 x $190/m3 = US$2.28 billion

Indicative price data for the year 2020:

- 2020 Log Price: US$190 per cubic meter

- 2020 Sawn Timber Price: US$440 per cubic meter

6.4 Financial Returns

Financial Case Studies:

These financial case studies offer insights into the industry returns and provide an overview of investment opportunities and returns in the timber sector:

Case 1: Feasibility for a large-scale (50,000 hectares) private investment in timber plantation development in Indonesia indicated an Internal Rate of Return (IRR) of 14.12%.

Case 2: In the 2017 global timber investments report, IRR for Borneo ranged from 10% to 19%, highlighting the potential returns in the region.

Case 3: The Timber Association of Sabah presented a financial projection for a 400,000-hectare tree plantation with a 10-year rotation. This plantation was estimated to produce:

- Chips logs: US$146 million per annum.

- Sawlogs: US$98 million per annum.

- Veneer logs: US$178 million per annum.

Additionally, these logs would generate added value for midstream industries:

- Wood chips: US$300 million per year.

- Sawn timber: US$200 million per year.

- Veneer: US$460 million per year.

Further downstream industries, including cross-laminated timber, glued laminated timber, laminated veneer lumber, furniture, construction timber, building frames, and other applications, were anticipated.

The total income from both upstream and downstream activities was projected to be US$2.7 billion per year, with annual replanting costs at US$123 million on the rotation cycle.

Case 4: Reforestation for pine in the USA in 2019 showed a Return on Investment (ROI) of 9-11%.

Case 5: A hardwood plantation study in New England, Australia, conducted in 2002, estimated a value of US$23,143 per hectare for Year 35 in 2021, with an IRR of 7.5%.

These case studies provide valuable benchmarks and insights into the potential financial returns and investment opportunities within the timber industry, showcasing a range of IRRs and ROIs across different projects and regions.

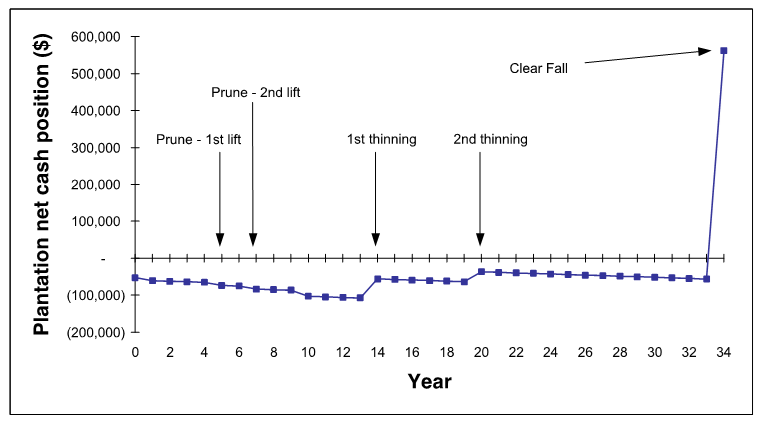

Cash flow projection hardwood plantation Australia

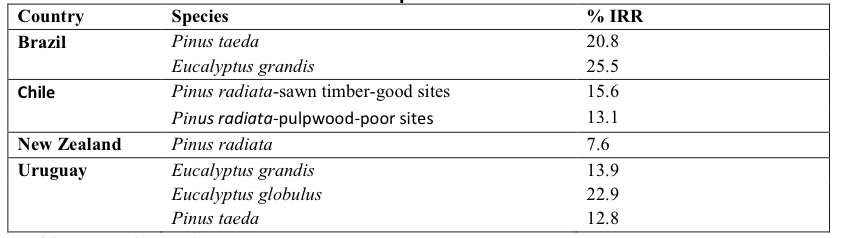

Case 6: 2009 study of IRR for selected countries and species

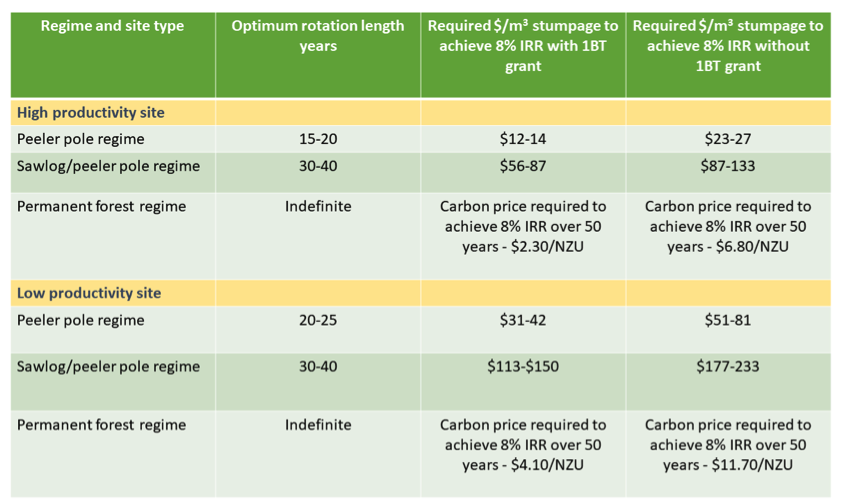

Case 7: Outcomes of an economic model for 8% IRR

Case 8: Timber investment returns 2015–2020, without land prices.

Eucalyptus IRR: 7.5% – 31.5%

Source: Chudy RP and Cubbage FW. 2020.

2019 Financial Income of listed local timber companies.

Source: https://www.wsj.com/market-data/quotes/company-list

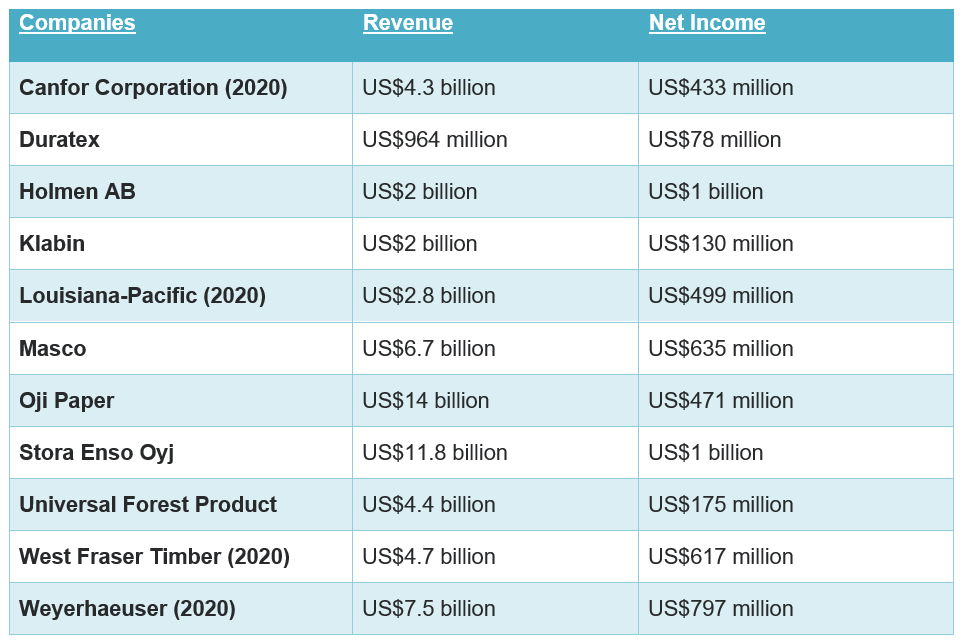

2019 Financial Income of listed international forestry companies

Source: https://www.wsj.com/market-data/quotes/company-list

6.5 Source of Funding

To support this ambitious timber plantation project, various sources of funding and stakeholders can be involved:

1. Strategic Investors:

- New Investor: A project leader group with a strong focus on business and financial management can provide capital and expertise.

- Financier: Agriculture private equity groups can contribute substantial funding for the project.

- Operator: International timber plantation operators with experience in managing large-scale timber plantations can partner in the project.

- Target Market: Local timber sawmill and downstream operators can invest and participate in the project, ensuring a direct market for the timber produced.

This diverse set of stakeholders can pool their resources and expertise tosecure the necessary funding for the project and ensure its successful execution.

2. Private Equities and Investors

Abrdn Investment Management Alecta Allstate Investments APG Asset Management Arrowstreet Capital Asset Management One AXA Investment Managers BlackRock Boston Partners Global Investors BTG Pactual Timber Investment Group Carnegie Funds Carlyle Group Cohen & Steers Capital Management Daiwa Asset Management Dasos Capital Dimensional Fund Advisors Eastspring Investments EBG Capital Ecotrust Evli Impact Forest Fund Fidelity Management & Research Fiduciary Management Finnfund First Eagle Investment First Trust Advisors Forest Enterprises Forest Investment Associates Franklin Mutual Advisers Fuller & Thaler Asset Management Geode Capital Management Global Forest Partners Green Diamond Gresham House Handelsbanken Hermes Investment Management Invesco Advisers J. D. Irving JPMorgan Investment Management Ketcham Investments Lyme Timber Lyxor International Asset Management Macquarie Investment Management Manulife IM Massachusetts Financial Services Mobilising Finance for Forest Molpus Woodlands Group New Island Group New Forests Group Nordea Funds Norges Bank Investment Management Nomura Northern Trust Investments OneFortyOne Partners Group Pictet Asset Management PotlatchDeltic Rayonier Resource Management Services RMK Timberland Group Sands Capital Management Schroder Investment Management SEB Investment Management Sierra Pacific Industries Solidium Oy SSgA Funds Management Stafford Capital Partners Stellex Capital Management Strategic Timber Trust Sumitomo Mitsui Trust Asset Management Swedbank Robur Funds T. Rowe Price Timber Investment Group Timberland Investment Resources Vanguard Group Wagner Forest Management Wellington Management Weyerhaeuser

3. Consultants, development and funding managers for the timber plantation industries:

Boston Consulting Group Durable Eucalyptus Growers’ Forum Ents Forestry Forest Business Network Forestry Consultants Forsci Global AgInvesting Global Forest Partners Global Forestry Services Greenwood Strategy Heartwood Plantations KPMG LMC International Margules Groome McKinsey & Company NZ Dryland Forests Initiative (NZDFI) Palico Parametric Portfolio Associates PF Olsen Plantation Management Partners Private Forestry Service Queensland Prequin RISI SGS Timber Capita Timber Investment Management Organisation (TIMO)

6.6 Where’s the Big Opportunity?

The big opportunities lie in various aspects of the timber industry:

- Timber Downstream: The downstream segment of the timber industry, including sawmill businesses, construction, and export furniture industries, often provides a higher return compared to plantation timber logs at farm gate prices. This sector benefits from processing and value addition. Here are some indicative 2021 prices for timber products in Sabah and Sarawak:

- Hard Logs: US$269 per cubic meter

- Sawn Timber: US$535 per cubic meter

- Plywood: US$1,996 per cubic meter

- Veneer: US$1,638 per cubic meter

- Forest Carbon Credits: The growth of forest carbon credit markets has been remarkable, driven by the increasing demand for carbon offsets from corporations and governments committed to reducing their carbon footprint. In 2022, the voluntary carbon market’s traded value was estimated at around US$980 billion, with forest carbon credits playing a substantial role. Well managed forest carbon credits are seen as a crucial tool in the urgent fight against climate change. This presents a significant financial opportunity for sustainable forestry projects that can contribute to carbon sequestration and offsetting.

These opportunities highlight the potential for not only timber production but also value-added downstream activities and environmental benefits through carbon credit initiatives. Exploring these avenues can enhance the financial and environmental sustainability of the timber plantation project.

7.0 Management Team

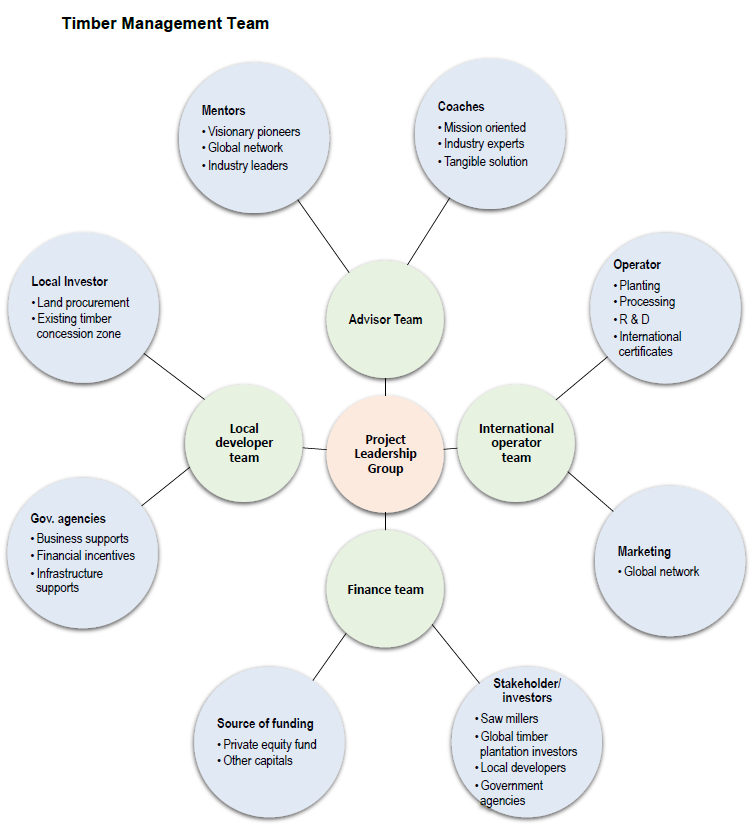

7.1 Key management team

- Mentor:

Mentors are visionary pioneers and industry leaders with a vast global network. They provide invaluable guidance and inspiration.

- Coaches:

Coaches are mission-oriented industry experts who offer practical solutions to challenges, ensuring the team stays focused on its objectives.

- Partners:

1. An established global timber plantation group that will help to set up the international best practice and standards for the local timber industry.

2. A reputable financier with access to sources of funding and exerts a responsible financial framework for the project.

3. A team of experienced operation managers in plantation, milling, local timber industry network and procurement of resources.

4. A credible government agency that has the vision, transparency and authority to implement the international benchmark.

In the timber plantation industry, several global leaders have made significant contributions, shaping its growth and success. Here is a list of some of these remarkable individuals, honoured for their vision and dedication:

- Professor Grahame Applegate

- David Brand

- Pat Groenhout

- Alex Lindsay

- Glen MacNair

- Paul Millen

- Dr John Turner

- Ricardo Vilela

- Norman Wong

These are just a few of the outstanding professionals and captains of the industry. The readers are encouraged to explore further and conduct their research to learn more about the management teams in this dynamic field.

7.2 Key Management Team Model

8.0 Unique Business Model

The timber plantation project proposes a unique and comprehensive business model that draws inspiration from successful models in Australia and New Zealand. This model encompasses various elements aimed at ensuring the project’s success and sustainability:

8.1 Successful Track Record

- The project takes inspiration from the successful Eucalyptus plantation models in Australia and New Zealand, which have achieved success across the upstream and midstream industries.

- Strategic alignment with Australian and New Zealand timber industry stakeholders, such as Private Forestry Service Queensland (PFSQ) and New Zealand Dryland Forests Initiative (NZDFI), will enhance project performance and productivity.

8.2 Entry Model:

- The project plans to establish the tree plantation through leasing existing timber concession zones, allowing for rapid market entry.

- Strategic partnerships with government bodies, industry players, landholders, and local communities offer multiple benefits, including support with licensing and approval processes, lower investment capital requirements, risk diversification, alignment with industry stakeholders, community acceptance, and reduced market entry costs.

8.3 Unique Business Model:

- The project aims to form strategic partnerships with a well-known financial service provider and an internationally reputable timber group. These partnerships will signify the host government’s commitment to reforestation in Borneo Island, enhancing the project’s image and branding.

- The unique business model emphasizes full integration and commitment among stakeholders with aligned goals, ensuring transparency and efficiency.

- Key benefits of this model include assurance of timber quality, specified volume, and pricing structure for saw millers and buyers, set parameters for quantity and cost for the producer, investor confidence in meeting business and financial expectations, rapid market entry through buying or leasing existing plantation concession land, and high-quality plantation management by an international specialist group focused on Eucalyptus plantation.

This comprehensive and integrated business model is designed to not only maximize the success of the timber plantation project but also foster sustainable practices and positive partnerships with various stakeholders.

9.0 Key Success Factors & Risk Mitigation

The success of the timber plantation project is influenced by several key factors, and careful risk mitigation measures are essential for its sustainability:

9.1 Key Success Factors:

- Ready Market: A strong and ready market with robust demand from local wood product industries is a crucial success factor.

- High-Quality Silviculture and Management: Implementing high-quality silviculture and forestry management practices, along with ongoing research and development for continuous improvement, is essential.

- Suitable Topography and Soil Conditions: Securing plantation land with suitable topography and soil conditions is vital. Ensuring a reliable supply of quality planting stock for the nursery is also critical.

- Compliance with Certification Programs: Focusing on compliance with local and international forest certification programs, such as PEFC and FSC, demonstrates commitment to sustainable forest management.

- Government Support: Strong government support, including taxation incentives, subsidized loans, concession grants, and fast-track approval programs, is necessary for the success of timber plantation projects.

- Acquisition of Existing Concession Forestland: Acquiring existing concession forestland is an effective method for rapid market penetration and project success.

- Strong Management Team: Having a strong management team with operational experience and a network in the industry is a key formula for successful investment.

9.2 Risks:

- Fire, Pest, and Disease: Risks associated with fire outbreaks, pest infestations, and diseases can impact the health of the plantation and timber production.

- Land Issues: Land-related issues, including disputes or challenges to land ownership or usage, can pose risks to the project.

- Price Fluctuation: Price fluctuations in the timber market can affect the project’s financial performance.

9.3 Risk Mitigation:

- Active Forest Management: Actively engaging in forest management with established benchmark practices helps mitigate risks related to fire, pests, and diseases.

- Government and Community Support: Strong support from the government, local industries, and the community can help mitigate various risks, including land issues.

- Price Resilience: Timber plantations have the advantage that, if timber prices are low at a particular point in time, trees will continue to grow, providing the opportunity to wait for more favourable market conditions.

10.0 Exit Strategy

An exit strategy is a crucial component of any investment plan. Here are the elements of the exit strategy for the timber plantation project:

10.1 Forms of Exit:

- IPO (Initial Public Offering): Investors can sell their shares as part of the IPO to the public.

- M&A (Merger and Acquisition): The project can be strategically acquired by another company in the timber industry.

- Sale: Private investors have the option to sell their stake to another private equity firm.

- Buyback: Management of the company can choose to buy back the equity stake from the private investors.

10.2 Benefits of the Business to New Investors:

- Market: New investors can tap into a ready target market of sawmill companies in Borneo.

- Revenue: The project offers recurring revenue with planned future growth.

- Price: Rising tropical timber log prices due to a supply shortage can benefit new investors.

- Risk: Secure demand reduces risk exposure to commodity price fluctuations.

- Product: New product lines can expand into the downstream saw timber industry.

- Opportunity: Investors can capture new opportunities in downstream finish timber products that generate additional revenue.

- Exit: The timing of the exit can be flexible and can occur at different stages of growth, with longer investment years potentially yielding greater revenue and higher returns.

10.3 Attraction of the Business to New Investors:

- Market: New investors can capture additional market share in the regional timber industry.

- Cost: Acquiring the business can enhance economies of scale and reduce costs.

- Leadership: New leadership teams can redefine and improve business and financial strategies.

- Distribution: Access to new markets, new products, and new distribution channels can be appealing.

- Revenue: There is potential for additional revenue from future downstream timber products in export markets.

10.4 Winning Strategy:

- ESG (Environmental, Social, and Governance): A sustainable timber plantation aligns with ESG policies, providing long-term growth prospects.

- Win-Win: The project offers a profitable business model with significant potential for downstream products. Additionally, it contributes to soil improvement, wildlife protection, the prevention of illegal logging, and job security for local communities.