“There is treasure to be desired and oil in the dwelling of the wise; but a foolish man spendeth it up.”

Proverbs 21:20 (KJV)

Question: What is the difference between extra virgin olive oil and cooking palm oil?

Answer: About US$4/kg

2021 Supermarket prices from Australia and Malaysia

What is Your Purpose in Work?

- Halting Environmental Harm: One purpose is to put an end to the distressing killing of pygmy elephants in oil palm plantations of Borneo. The new stakeholders can be the guardians of these majestic creatures.

- Sustainable Practices: The aim is to cease unsustainable oil palm plantation practices, thereby preventing further degradation of tropical forests and the peat environment.

- Supporting Workers: Another key objective is to end the exploitation of farmworkers in this industry, ensuring fair wages and humane working conditions.

- Investing in Sustainability: By investing in sustainable oil palm plantations, the stakeholders can be instrumental in bringing positive change to Borneo Island and beyond.

What Drives Your Corporation’s Core Value?

- Innovative Business Models: Visionary company is always seek to identify and implement innovative business models that have the potential to disrupt the palm oil industry’s value chain, leading to transformative changes.

- Feeding the World: The mission is grander than just profits; it’s about making a substantial contribution to providing affordable edible oil to underdeveloped and developing nations. The mission is to feed three billion people every day.

When the purpose of your work aligns with the mission of your corporation, a powerful synergy emerges. This union empowers us to make impactful decisions, such as conserving wildlife, promoting sustainable practices, and taking a leading role in the edible oil industry. In essence, it’s not just about the oil; it’s about the wisdom to recognize the treasure in the actions and the commitment to utilize it for the betterment of this planet and its inhabitants.

Mum and baby Pygmy Elephants

1.0 Executive Summary

Mission

- The mission is to invest in 400,000 hectares of sustainable oil palm plantations and mills to produce 2 million metric tons of crude palm oil (CPO).

- Initial stage is to invest in 40,000 hectares of sustainable oil palm plantation along with four 60-100 metric tons fresh fruit bunch (FFB) per hour sustainable palm oil mills. This phase aims to produce 200,000 metric tons of CPO annually, primarily targeting the markets in India and China.

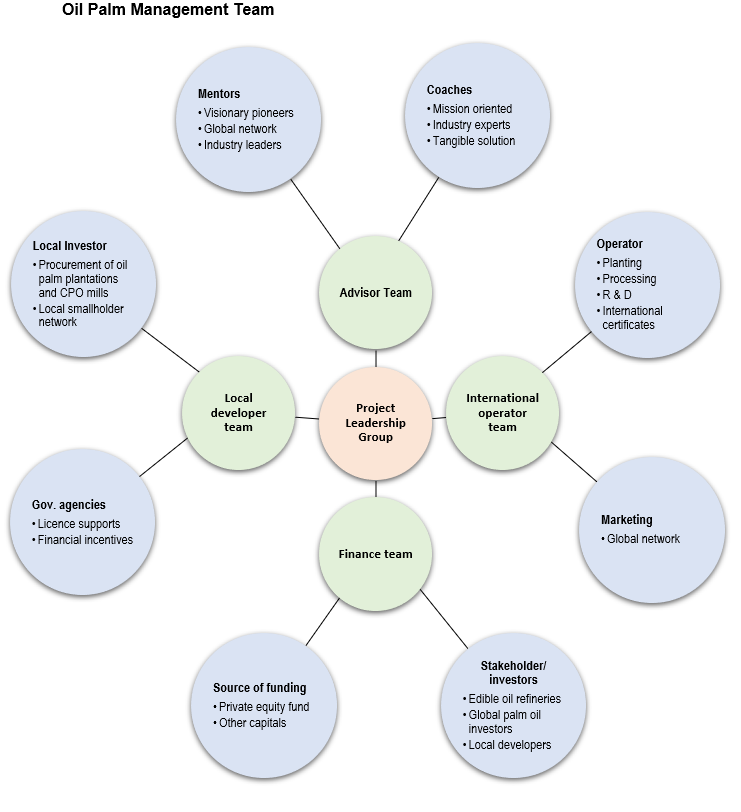

Key management team

- Mentors: Visionary pioneers and industry leaders who offer invaluable guidance and inspiration, leveraging their extensive global networks.

- Coaches: Mission-oriented industry experts providing practical solutions to challenges, ensuring the team remains focused on its objectives.

- Partners:

- A project leader with a strategic vision to organize a disruptive model.

- A reputable financier with access to diverse funding sources.

- A team of experienced operation managers specialising in plantation, processing, and an extensive global industry network, along with expertise in procuring local resources.

Product benefits

- Palm oil is an attractive choice due to its cost-effectiveness and versatility in applications.

- Oil palm is exceptionally productive, yielding 5-10 times more per hectare compared to the 10 major oilseed crops.

- Its popularity stems from high heat resistance, long shelf life, and competitive pricing.

- Borneo offers ideal conditions for oil palm plantations, boasting the world’s highest fruit yields per hectare.

- Sustainability certification contributes to a 2% higher profit margin.

Target market

- The primary markets are India and China, both of which annually import 9 million metric tons and 7 million metric tons of palm oil, respectively.

- Key customers are the oil processors in these two countries.

Financial projections

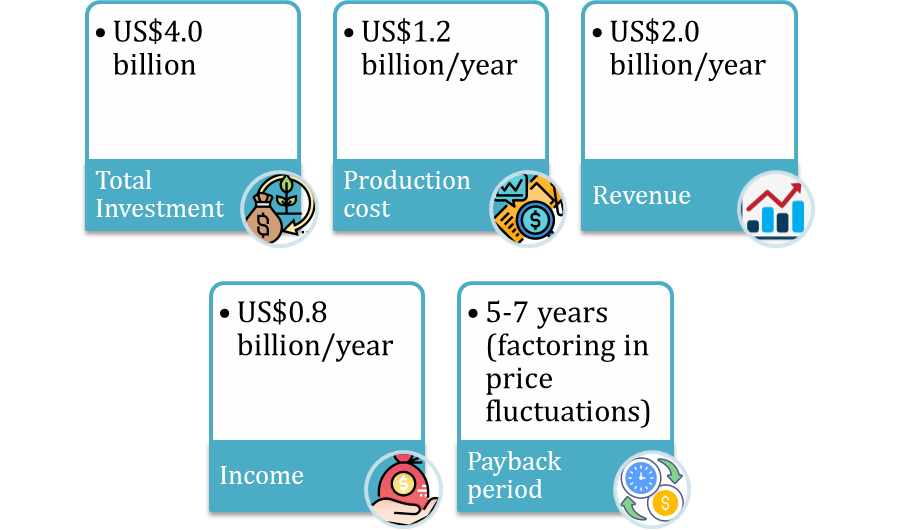

- Total investment: US$4.0 billion

- Production cost: US$1.2 billion/year

- Revenue: US$2.0 billion/year

- Income: US$0.8 billion/year

- Payback period: 5-7 years (Allow for price fluctuation)

Unique business model

- Exclusive offer end buyers specific volume and pricing structures.

- Producers set parameters for quantity and cost structures.

- Stakeholders share in the profits.

- Private equity fund investors have assurance regarding business and financial expectations.

- The entry model involves purchasing existing plantations with mills, providing immediate cash flow and stable income.

- The strategy includes implementation of a vertical and horizontal integration model from farm gate to retail operations.

- The aim is to lead the oil palm industry in both best practices and profitability.

2.0 Mission

2.1 Problem

Oil palm plantations have had a detrimental impact on rainforests and wildlife habitats. The extinction of the Sumatran rhino in 2019 on Borneo Island, where they once thrived, is a tragic example. Malaysia has officially lost this unique species. Over the past decade, 60 pygmy elephants have perished due to poisoning and illegal culling within oil palm plantations.

Moreover, unsustainable practices in oil palm cultivation have led to the degradation of tropical forests, damage to peat environments, and the exploitation of farmworkers.

The demand for edible oil, driven by India and China, is soaring as they prioritize food security at competitive prices. Surprisingly, neither of these countries currently boasts large-scale oil palm plantations.

2.2 Solution

To address these pressing issues, the following solutions are proposed:

- Strategic Alignment: Forge strategic partnerships with processors in India and China to meet their growing edible oil demands effectively.

- Invest in Oil Palm Plantations: Recognize that oil palm is the leading edible oil crop globally, offering the lowest production costs and the highest yields. Investing in this crop is a viable solution.

- Optimal Location: Borneo emerges as the prime location for this endeavour. Situated between 5 degrees north and south of the equator, the island boasts vast agricultural land, abundant sunshine, ample rainfall, and direct access to the Asia Pacific market.

- Sustainable Practices: Advocate for investment fund guidelines, buyer specifications, and production policies that align with the Roundtable on Sustainable Palm Oil (RSPO) and No Deforestation, No Peat, No Exploitation (NDPE) frameworks.

2.3 Mission

Phase 1:

Initiate the project by investing in 40,000 hectares of oil palm plantation land, accompanied by the establishment of four 60-100 metric tons per hour palm oil mills. This initial phase aims to produce 200,000 metric tons of Crude Palm Oil (CPO) to cater to the demands of the China and India markets.

Phase 2:

Expand efforts by committing to 400,000 hectares of oil palm plantation and additional palm oil mills. This expansion is projected to yield 2 million metric tons of CPO for export markets.

Phase 3:

Diversify and add value by investing in downstream industries through strategic partnerships in India and China. This phase aims to strengthen the overall supply chain and enhance the sustainability of the venture.

3.0 Product

3.1 Product Description

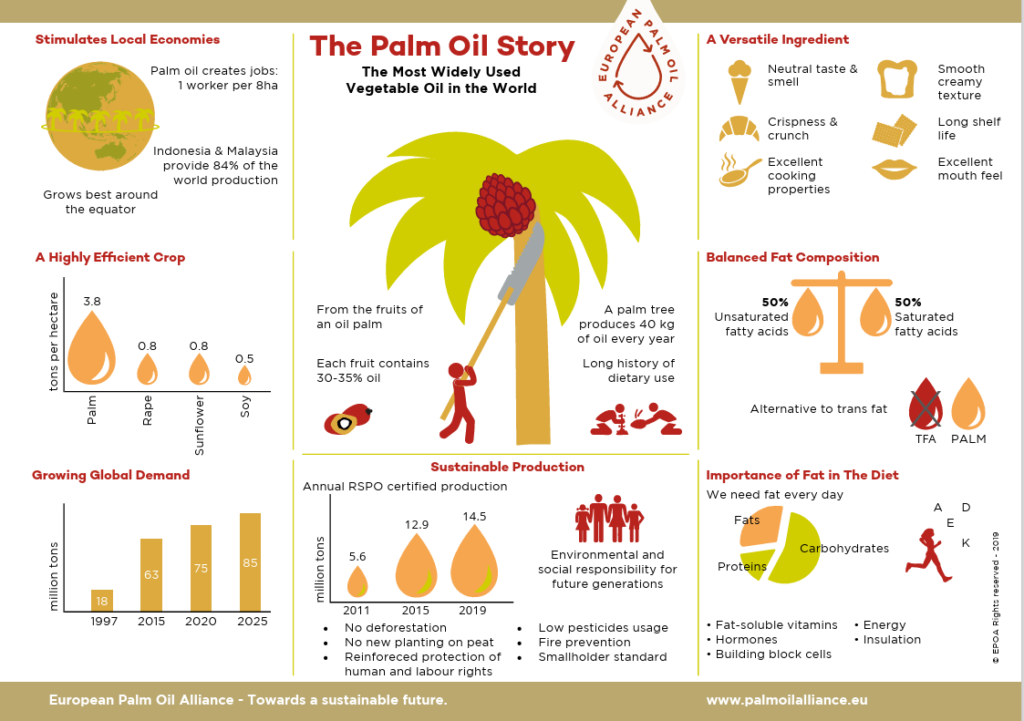

Palm oil is a tropical vegetable oil extracted from the fruits of the oil palm tree. Its versatile applications span the food, oleochemical, biomass fuel, pharmaceutical, animal feed, and various derivative product industries. Notably, it ranks as the world’s most consumed edible oil. The oil palm tree stands out as the most productive oilseed globally, with a remarkable capacity to yield between 5 to 11 metric tons of crude palm oil (CPO) per hectare.

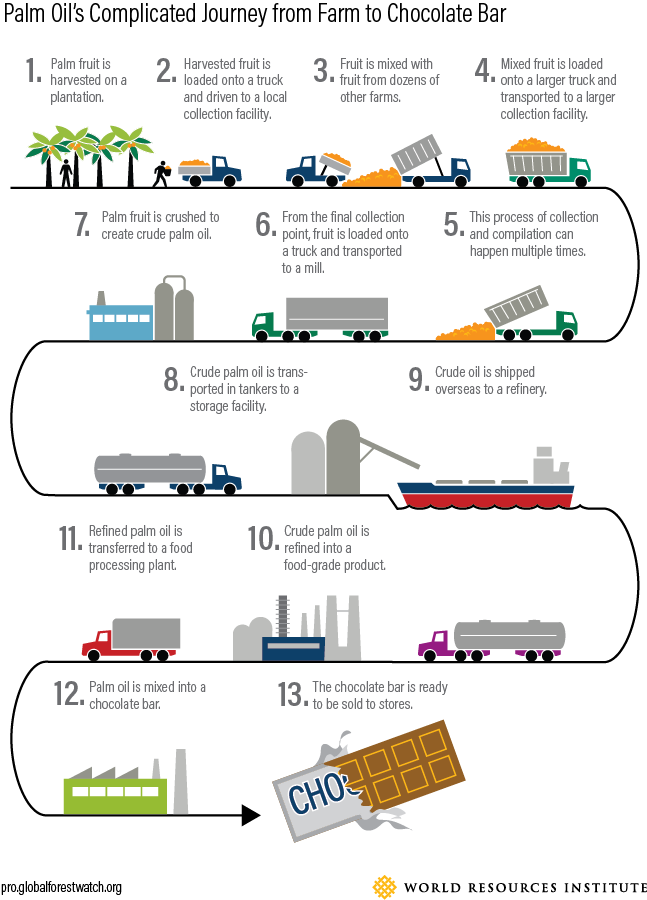

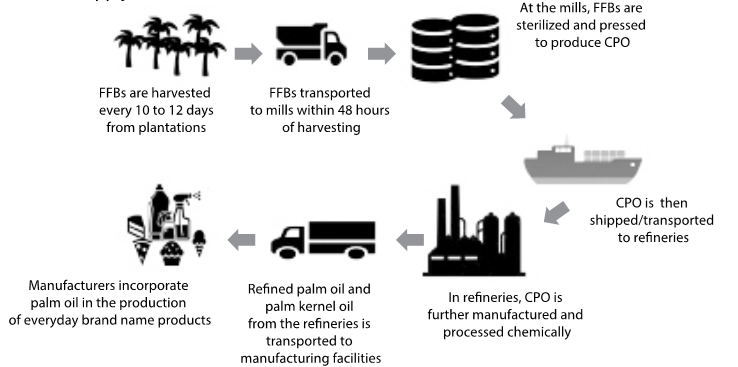

Palm tree to food

3.2 Product Attributes

Oil palm cultivation demonstrates remarkable efficiency, demanding relatively small quantities of energy, fertilizers, and pesticides. It boasts the highest oil yield per hectare compared to any other vegetable oil source. Specifically, Borneo takes the lead with a production rate ranging from 5 to 11 metric tons per hectare, surpassing the global average of 3.5 metric tons per hectare. Furthermore, the oil palm tree begins fruiting in its fourth year and continues to bear fruit throughout the year, with replanting typically occurring around the 25th year.

Oil Palm Plantation

Oil Palm Fruit Bunch

Palm Oil & Palm Kernel Oil

3.3 Product Benefits

- Cost-Efficiency: Palm oil stands out due to its lower production costs and its adaptability across various applications.

- Exceptional Yield: Among the top 10 major oilseed crops, oil palm is 5-10 times more productive per hectare, making it highly sought after.

- Versatility: Palm oil’s popularity derives from its high heat resistance, extended shelf life, and competitive pricing, making it a preferred choice for food manufacturers.

- Industry Familiarity: Palm oil enjoys widespread recognition and utilization within the food industry.

- Sustainability: Well-managed palm oil plantations can incorporate wildlife protection programs, contributing positively to the tourism sector.

- Profit Margin: Achieving sustainability certification leads to a 2% higher profit margin.

Palm oil features Palm oil yields

3.4 Product Competitive Advantages

- Location: Oil palm thrives in conditions of high humidity (80-90%), warm temperatures (29-30°C), and evenly distributed annual rainfall of 2000-2500 mm. Borneo offers the most conducive environment for oil palm cultivation globally, resulting in the highest fruit yields per hectare.

- Market: Borneo Island’s strategic central location within the Asia Pacific region grants direct access to target markets, enhancing market competitiveness.

- Cost-Efficiency: Borneo’s vast frontier land, lower energy tariffs, and a substantial pool of local farmworkers contribute to competitive production costs.

- Yield: Borneo Island’s outstanding agricultural conditions translate into a higher yield of 5-11 metric tons per hectare of CPO, reinforcing its position as an ideal location for oil palm cultivation.

4.0 Market

4.1 Market Segments

The palm oil market is divided into two primary segments: edible oil and industrial applications. Edible oil accounts for approximately 80% of palm oil consumption, while the oleochemical sector utilizes about 15%, and biofuel makes up 2% of the market.

The largest consumers of palm oil globally are Indonesia, India, the European Union (EU), and China, collectively responsible for half of the world’s palm oil consumption. In 2020, total edible oil production reached 209 million metric tons, with palm oil commanding the lion’s share at 35%, totalling 73 million metric tons. Indonesia and Malaysia are the top producers of crude palm oil (CPO), supplying 83% of the world’s total, with 42.5 million metric tons and 19 million metric tons, respectively. The palm oil industry is projected to reach a market value of US$83 billion by 2027.

4.2 Target Market Segment Strategy

The regions showing the highest demand growth for palm oil are Indonesia, India, China, and the EU, with India and China emphasizing food security as a top priority. The strategic approach is to invest in palm oil plantations equipped with CPO mills, as these segments offer the most attractive margins within the value chain. Refineries located in these target markets will import CPO and process it to create end products.

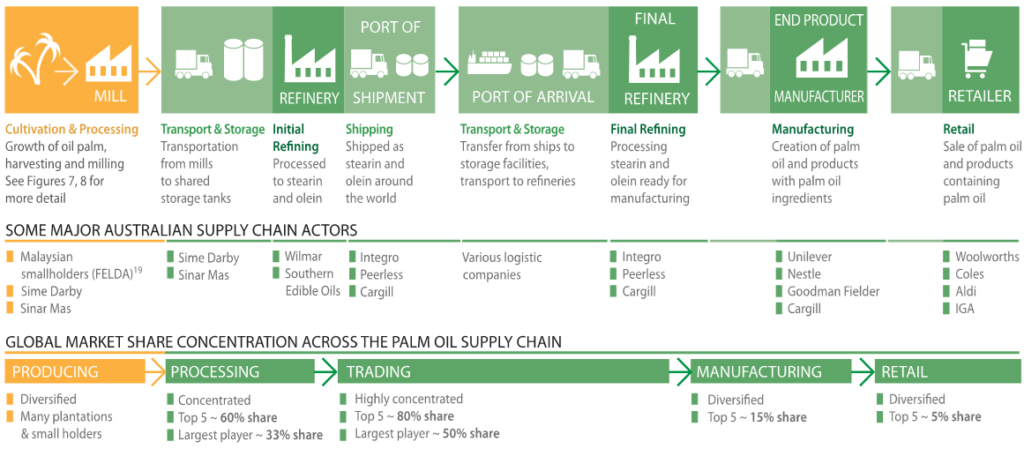

Palm oil supply chain-Australia

4.3 Market Needs

- The global consumption of vegetable oil in 2020 reached 209 million metric tons.

- Demand is projected to grow to 234.5 million metric tons by 2027.

- Edible oil consumption constitutes 80% of the vegetable oil market.

- Palm oil production reached 74.2 million metric tons and is expected to increase to 83.2 million metric tons by 2027.

- Developed countries’ edible oil consumption was 53.9 million metric tons in 2020 and is forecasted to rise to 55.2 million metric tons by 2027.

- Developing countries’ edible oil consumption was 155.7 million metric tons in 2020 and is anticipated to climb to 179.5 million metric tons by 2027.

4.4 Growth Drivers

Three key factors drive growth in the global edible oil market: population growth, rising incomes, and dietary shifts. In Asia, per capita consumption of oils is currently at 23 kg per year, compared to 37 kg per year in Western nations. Palm oil anticipates a stable growth trajectory, increasing from 74 million metric tons in 2020 to a projected 83 million metric tons by 2027, fuelled by population growth, rising consumption, and the expanding affluent middle class.

Additionally, demand from the Middle East nations is on the rise, with these countries importing 55% of their edible oil. Another significant demand driver is the biomass fuel sector, with the Indonesian government planning to increase palm oil content in biodiesel by 50%. Malaysia is also considering the production of palm oil-based jet fuel within the next five years, with government funds allocated for research into palm oil derivatives as aviation fuel feedstock.

4.5 Key Customers

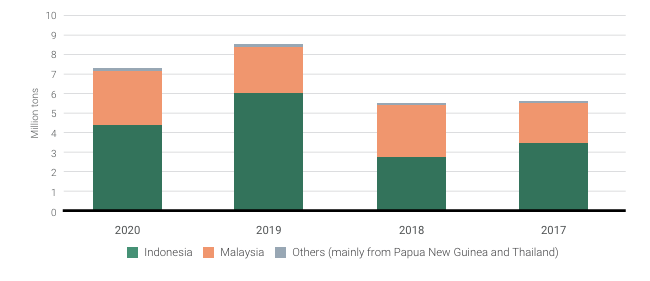

- India’s annual palm oil demand stands at 9 million metric tons, with 5 million metric tons supplied by Indonesia and 4 million metric tons from Malaysia.

- China imports 7 million metric tons of palm oil annually, with 4 million metric tons coming from Indonesia and 3 million metric tons from Malaysia.

China palm oil imports 2017–2020

China: Top palm oil processors in China

- Yihai Kerry Arawana Holdings

- Yizheng Fangshun Oils & Grains Industry

- COFCO Oils and Oilseeds

- Sinograin Zhenjiang Grain and Oil

- Guangzhou Zhizhiuuan Oil Industry

- Guangdong Yingma Food

- Xiamen Zhongsheng Grain and Oil Group

- Henan-ichoose Oils

- Fujian Huaren Oils and Fats

India: Top palm oil brands in India

- Ruchi Soya Industries

- Cargill India

- Godrej Agrovet

- Adani Wilmar

- Edible Group

- FFF Industries

- KM Oil Industries

- ALR Trading

4.6 Competition and Industry

1. Largest market share

Palm oil holds the distinction of being the most produced oil globally, commanding the largest share in the edible oil market. In terms of world edible oil production, palm oil accounts for 35%, surpassing other oils like soybeans at 26%, canola at 15%, sunflower at 9%, with the remaining 15% attributed to various other sources.

2. Yield

When it comes to oil yield, oil palm plantations in Borneo boast the highest production rate, ranging from 4.7 to 11 metric tons per hectare (mt/ha). This surpasses the global production rate of 3.5 mt/ha for oil crops. Palm oil’s exceptional productivity is further underscored by its ability to offer 10 times the oil yield, producing an average of 4.03 mt/ha. In comparison, competitors like soybeans, sunflower, and rapeseed offer annual oil yields of 0.43 mt/ha, 0.65 mt/ha, and 0.76 mt/ha, respectively.

3. Land

While suitable land for oil palm cultivation can be found in various regions, Borneo emerges as an optimal choice. Here are some considerations for other potential regions:

- Amazon Region: This region has suitable land but is hindered by challenges related to soil drainage and acidity.

- Central Africa, Congo Basin, and Coastal Western Africa: Although these areas have potential, they face limitations due to local dry seasons and gravelly soils. Expansion opportunities are restricted due to land scarcity, unskilled labor, and inadequate infrastructure.

In contrast, Borneo offers extensive oil palm plantations and ample land for future development, making it a preferred choice for the industry.

Oil Palm in Sabah

4. Leading palm oil companies in Malaysia, Singapore and Indonesia:

Able Perfect ADM Agro Mandiri Semesta Plantations (Ganda Group) Anglo-Eastern, ANJ (Austindo) Apical Asian Agri (Royal Golden Eagle) Astra Agro Lestari (Jardine Matheson) Bell Group Austina Nusantara Jaya Bakrie Batu Kawan (KLK) BLD Plantation Boustead Plantations Bumitama Agri (Harita) Bunge Cargill Carotino Darmex Agro Dharma Satya Nusantara Eagle High Plantations (Prajwal) Far East Holdings FGV (Felda) First Resources (Surya Dumai) Genting Plantations Glenealy Plantations Golden Agri-Resources (Sinar Mas) Green Ocean Group Hap Seng Plantations Hayel Saeed Anam Group Innovans Palm Industries IJM Plantations IOI Group Itochu Jardine Matheson Jaya Tiasa Holding Kencana Agri KPN Plantation KL Kepong Kim Loong Resources Kretam Holdings Kulim, LDC London Sumatra Indonesia Muhibah Palm Product Musim Mas Nusantara Olam Group, Perkebunan Permata Hijau Group Rimbunan Sawit Salim Ivomas Pratama Samling Group Sampoerna Agro Sarawak Oil Palms Sawit Sumbermas Sarana Sime Darby Sina Mas Socfin Group Southern Edible Oil Ta Ann Holdings Taner Tradewinds Plantation TSH Resources Tunas Baru Lampung Unilever United Plantations Wilmar Yee Lee

The largest conglomerates involved in production, processing and trade of palm oil:

Cargill FELDA GAR (Golden Agri Resources) IOI Group Musim Mas Sime Darby Wilmar

Organisation

FAO (Food and Agriculture Organisation of the United Nations) FOSFA (Federation of Oils, Seeds and Fats Association) IOPRI (Indonesian Oil Palm Research Institute) IPOA/GAPKI (Indonesia Palm Oil Association) ISPO (Indonesian Sustainable Palm Oil) MPOB (Malaysian Palm Oil Board) MPOC (Malaysian Palm Oil Council) MSPO (Malaysian Sustainable Palm Oil) PORIM (Palm Oil Research Institute of Malaysia) PRI (Principles for Responsible Investment) RSPO (Roundtable on Sustainable Palm Oil)

5. Strong Opposition

Land: One of the most significant challenges faced by the palm oil industry is strong opposition from developed nations. This opposition primarily centres around concerns related to land use. Critics argue that palm oil plantations compete with and often encroach upon wildlife habitats and vital rainforests, leading to deforestation and habitat loss.

Competitor: Palm oil’s biggest rival in the edible oil market is soybean oil. The competition from soybean oil significantly impacts the demand and prices of palm oil. The soybean oil industry has established itself with a well-developed infrastructure, substantial investment in research and development (R&D) for plantation, processing, and marketing, making it a formidable competitor in the edible oil market.

4.7 Borneo’s Competitive Advantages

Land:

Borneo, situated between 5-7 degrees north and south of the equator, presents one of the most favourable environments for oil palm plantations. The region benefits from abundant rainfall and consistent sunshine, creating optimal conditions for palm oil cultivation.

Species:

Borneo has access to modern palm oil varieties with early maturity and high-yielding breeds capable of exceeding 5-11 metric tons per hectare per year, outperforming global averages.

Experience:

With over six decades of experience, Borneo has honed its expertise in every aspect of the palm oil industry, including plantation management, processing, refining, and international trade.

Cost:

The region enjoys lower production costs compared to many other palm oil-producing areas, contributing to its competitiveness.

Support:

Borneo benefits from extensive government support and infrastructure investments designed to bolster the palm oil industry, creating a conducive environment for growth and development.

Location:

Borneo’s strategic central location in the heart of Asia provides it with easy access to key markets, including India and China, enhancing its position as a vital hub in the palm oil trade.

5.0 Operation

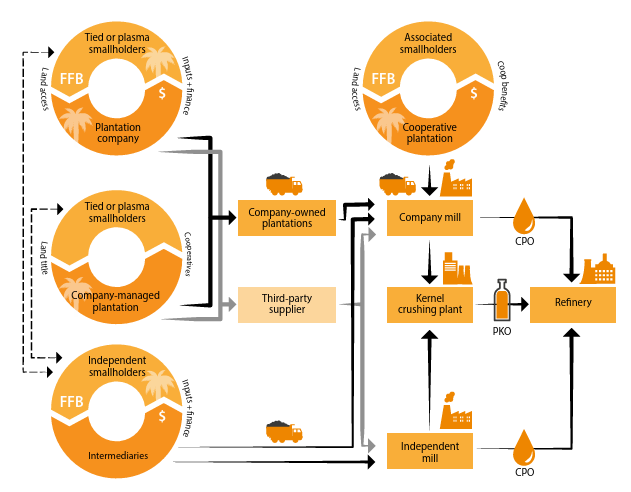

Palm oil supply chain

Plantation operation

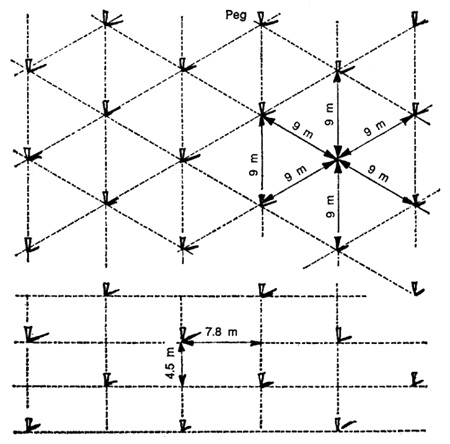

5.1 Nursery: 3-month 5.2 Planting in an open 5.3 Spacing

field: 6 months

5.4 Young Palm Tree 5.5 FFB Fruiting 5.6 Harvest

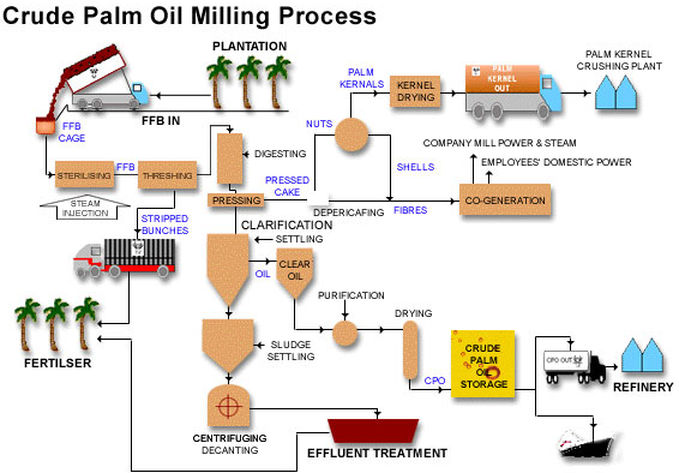

5.6 CPO (Crude Palm Oil) milling process

6.0 Financial Implications

6.1 Investment Segments

Investment in the palm oil industry encompasses three key segments:

- Upstream: Involves planting, cultivation, and harvesting.

- Midstream: Encompasses activities such as crushing, refining, and processing.

- Downstream: Relates to the retail of end-products, branding, and industrial derivatives.

Returns on investment (ROI) for each segment vary:

- Well-managed upstream oil palm plantation operations can yield returns ranging from 15% to 50% on investment.

- Midstream processing operations typically generate returns around 15% to 20% for efficient refining operations.

- Downstream derivatives offer ROI ranging from 17% to 30%, contingent on the product portfolio.

Case Studies on Investment:

Investment in oil palm plantations and mills is influenced by various factors such as location, land title encumbrances, terrain, tree age, yield rates, and more. Some notable cases include:

- In 2021, a 10,121-hectare palm oil plantation in Kinabatangan was acquired for US$156 million.

- In 2020, a fully cultivated 1,174-hectare palm oil plantation in Kinabatangan was valued at US$23 million.

- In 2018, a 4,915-hectare palm oil plantation in Sandakan, equipped with a 75-tonne per hour palm oil mill, was acquired for US$100 million.

- Also in 2018, 5,531 hectares of plantation land, along with a 60-tonne per hour palm oil mill, were valued at US$108 million.

The mission is to invest in 400,000 hectares of oil palm plantations with accompanying palm oil mills to produce 2 million metric tons of Crude Palm Oil (CPO) for export markets. This is broken down into phases, with Phase 1 focused on 40,000 hectares of land with mills, Phase 2 expanding to 400,000 hectares, and Phase 3 involving investments in downstream palm oil industries in collaboration with strategic partners in India and China.

6.2 Production Cost

In 2020, the average total production cost of Crude Palm Oil (CPO) ranged from US$350 to US$550 per metric ton.

- Phase 1: Producing 0.2 million metric tons at an estimated cost of US$600 per metric ton results in an expense of US$120 million.

- Phase 2: Producing 2 million metric tons at an estimated cost of US$600 per metric ton results in an expense of US$1.2 billion.

Here are some specific case studies related to production costs, CPO prices, revenues, and financial returns:

Production Costs and CPO Prices:

- 2020:

- Fresh Fruit Bunch (FFB) production cost: US$72 per metric ton.

- Milling costs: US$19 per metric ton.

- Crude Palm Oil (CPO) production cost: US$390 per metric ton.

- 2019:

- FFB production cost: US$70 per metric ton.

- Milling costs: US$20 per metric ton.

- CPO production cost: US$363 per metric ton.

- 2018:

- FFB production cost: US$77 per metric ton.

- Milling costs: US$20 per metric ton.

- CPO production cost: US$394 per metric ton.

6.3 CPO Prices and Revenues

- Revenue projections for Phases 1 and 2:

- Phase 1: Producing 0.2 million metric tons at an assumed price of US$1,000 per metric ton results in revenue of US$200 million per year.

- Phase 2: Producing 2 million metric tons at an assumed price of US$1,000 per metric ton results in revenue of US$2 billion per year.

- Price fluctuations:

- Prices for CPO fluctuated between US$450 and US$1,336 per metric ton over the last five years.

- In 2020, the average price was US$667 per metric ton.

- In 2021, the average price was US$1,000 per metric ton.

- In 2022, the price spiked to US$1,336 per metric ton.

6.4 Financial Returns

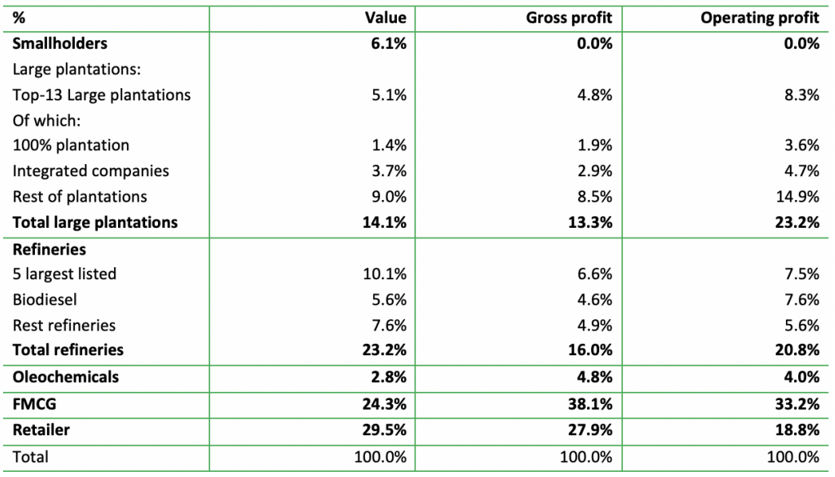

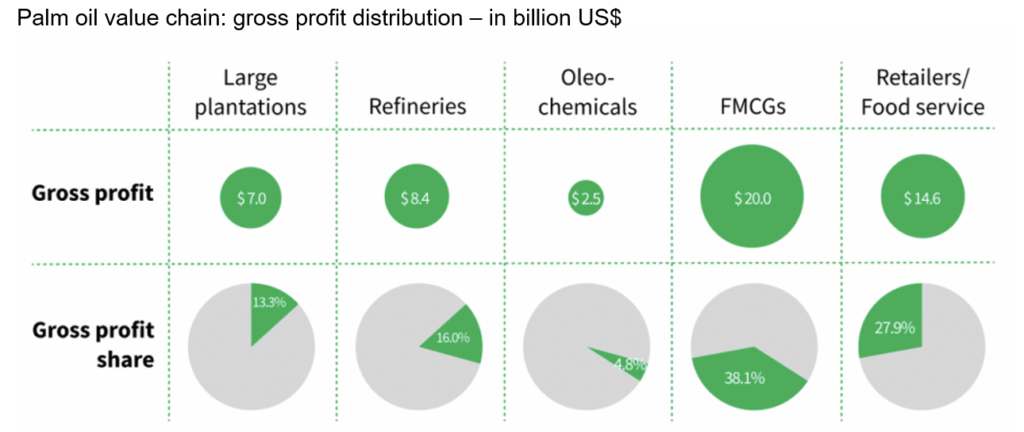

Palm oil value chain: value and profit margin

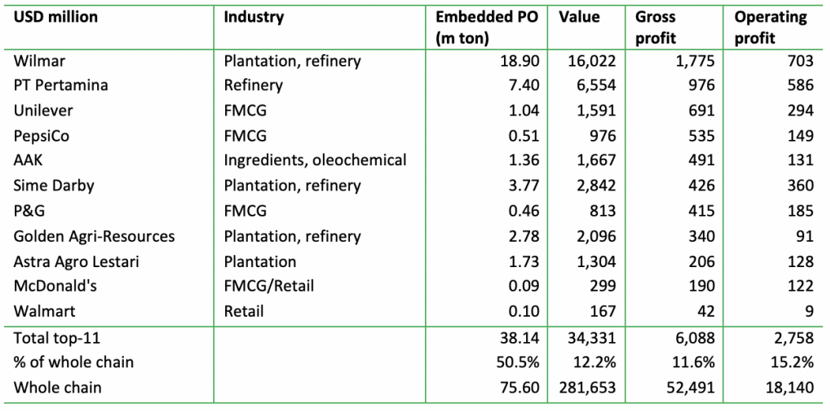

Palm oil value chain: Top 11 companies in value ranked by gross profit

The rate of return (IRR) depends on factors such as production cost, CPO price, and other parameters. Several successful case studies provide insights:

- Case 1 (2015): An 8,000-hectare plantation in Indonesia over 25 years resulted in an IRR of 14.83% and a payback period of 6.75 years.

- Case 2: A 2,500-hectare plantation over 25 years resulted in an IRR of 25% and a payback period of 7 years.

- Case 3: An estimation for Western Kalimantan suggested an IRR of 26% per annum over 25 years for oil plantations over 10,000 hectares.

- Case 4 (2011): The average CPO yield was 4.73 metric tons per hectare, with a production cost of US$340 per metric ton and an average CPO price of US$1,040 per metric ton, resulting in an average rate of return of US$2,900 per hectare.

- Case 5 (2018): A feasibility study for a 3,000-hectare palm oil plantation with a mill yielded an IRR of 29% and a payback period of 6.7 years for the plantation, along with an IRR of 17.89% and a payback period of 5.7 years for the palm oil processing plant.

These case studies illustrate the financial dynamics of the palm oil industry, emphasising the importance of factors like production costs and CPO prices in determining returns on investment.

2019 Financial Income of listed cassava dried chips companies.

Source: https://www.wsj.com/market-data/quotes/company-list

6.5 Source of Funding

1. Strategic Investors:

- New Investor: A project leader with a focus on business and financial management who brings capital and expertise to the project.

- Financier: Agriculture private equity groups specializing in funding agricultural ventures.

- Palm Oil Operator: International oil palm plantation and Crude Palm Oil (CPO) mill operators who may invest in expansion or new ventures.

- Target Market: Indian and Chinese palm oil refinery groups interested in securing a sustainable source of palm oil supply.

These strategic investors can provide the necessary capital and industry expertise to support the development and expansion of palm oil plantations and processing facilities.

2. Private equities and investors

ABRDN Achmea Investment Management ACTIAM ADM Capital Affirmative Investment Management Allianz Global Investors APG asset management Apollo Asia Fund a.s.r. Asset Management Aviva Investors AXA Investment Managers BlackRock BMO Global Asset Management BNP Paribas Asset Management Bright Ventures CalPERS Capfi Delen Asset Management China Investment Corporation China Southern Asset Management China Universal Asset Management CITIC Columbia Threadneedle Investments Credit Suisse Asset Management Dimensional Fund Advisors DONLINK Group Eastspring Investments EFund Management Federated Hermes Fidelity Investments First Sentier Investors Fullgoal Fund Management Generation Investment Management Green Century Capital Management HAID Group Harvest Fund Management Hillhouse Capital Management ING KBC Asset Management Kewalram Chanrai Holdings Kopernik Global Investors Lion Global Investors Liontrust Asset Management Louis Dreyfus Company Manulife Investment Management Massachusetts Financial Services McKinley Capital Management Mellon Investments NNIP Nomura Asset Management Northern Trust Investments Orbis Investment Management Principal Asset Management Quaero Capital Robeco Asset Management Schroders investment SEAF Segall Bryant & Hamill Silchester International Investors Société Financière des Caoutchoucs SSgA Funds Management Stanley-Laman Group Temasek Capital TIAA Investment Management UBS Asset Management Valu-Trac Investment Management Value Square Van Eck Associates Vanguard Group William Blair Investment Management

3. Other financial support to the cassava industries:

ADB ANZ Banque Degroof Petercam Luxembourg BCA BPDPKS (The Palm Oil Plantation Fund Management Agency) CDC Group CIMB Commonwealth Bank DBS Deutsche Bank HSBC IFC Mandiri Maybank Mitsubishi UFJ Mizuho New Zealand Superannuation Fund OCBC Public Mutual Rabobank RHB State Street Sumitomo Mitsui UOB

4. Consultants, development and industry specialists to the sustainable palm oil industries:

BCG Deloitte KPMG LMC International McKinsey & Company Ned Davis Research OFI (Oils & Fats International) PWC Sergi Enam Advisors Tropicrop Group

6.6 Where is the Big Opportunity?

The significant opportunity in the palm oil industry lies in the downstream segment of the value chain. This is where the potential for higher returns is most pronounced. By establishing strategic partnerships that encompass oil palm plantations, Crude Palm Oil (CPO) mills, refineries, and the retail market for cooking oil, a vertically integrated approach can be achieved.

Vertical integration in the palm oil industry allows for optimizing profit along the entire value chain. It enables control over various stages of production, processing, and distribution, ultimately leading to a more competitive cost structure and pricing strategy.

As of August 2021, the price dynamics in the industry are as follows:

- Crude Palm Oil (CPO): Priced at US$1,042 per metric ton.

- Cooking Oil: Priced at US$2,630 per metric ton.

These prices offer insights into the value potential within the palm oil downstream segment, particularly in the cooking oil retail market. Leveraging this opportunity through strategic partnerships and vertical integration can be a lucrative endeavour in the palm oil industry.

7.0 Management Team

7.1 Key Management Team

- Mentors: Visionary pioneers and industry leaders who offer invaluable guidance and inspiration, leveraging their extensive global networks.

- Coaches: Mission-oriented industry experts providing practical solutions to challenges, ensuring the team remains focused on its objectives.

- Partners:

- A project leader with a strategic vision to organize a disruptive model.

- A reputable financier with access to diverse funding sources.

- A team of experienced operation managers specialising in plantation, processing, and an extensive global industry network, along with expertise in procuring local resources.

In the palm oil industry, several global leaders have made significant contributions, shaping its growth and success. Here is a list of some of these remarkable individuals, honoured for their vision and dedication:

- Dr Retno Bos-Kusumaningtyas

- Neville Burman

- Mavath Chandran

- Dr James Fry

- Kuok Khoon Hong

- Dr Wong Kim Lian

- Martua Sitorus

These are just a few of the outstanding professionals and captains of the industry. The readers are encouraged to explore further and conduct their research to learn more about the management teams in this dynamic field.

7.2 Key Management Team Model

8.0 Unique Business Model

In the palm oil industry, a unique and successful business model has evolved over the past four decades. This model combines ownership and operation of upstream and midstream production systems, resulting in a comprehensive and efficient approach to the industry. This model has several key features:

8.1 Successful Track Record:

- Over the last 40 years, this model has demonstrated its success by integrating both upstream and midstream components.

- Ownership of oil palm plantations provides a stable and consistent supply of raw materials.

- The Crude Palm Oil (CPO) mill enhances profit margins within the value chain.

- The mill often buys additional fresh fruit bunches (FFB) from smallholders or traders through the plasma system, further strengthening the supply chain.

8.2 Entry Model:

- There are four common entry models into the palm oil industry:

- Agent/Distributor/Trading Partnerships

- Joint Ventures

- Direct Investment

- Acquisition

- Fully integrated vertical systems that include downstream segments are typically controlled by a few powerful industry players.

- Gaining licenses, permits, and access to target markets often involves navigating complex government regulations, setting high barriers to entry into the downstream segment.

- Acquiring existing oil palm plantations with CPO mills offers an effective entry strategy, providing immediate market access, cash flow, and minimal learning curves.

8.3 Unique Business Model:

- Sovereign nations prioritize food security, making edible oil production a top concern.

- India and China are exploring options to establish edible oil production in tropical regions, with Borneo Island serving as an ideal location for the initial stages of this endeavor.

- This unique business model aims to create a fully integrated system from farm gate to the retail market, aligning all stakeholders toward common goals.

Stakeholders of the Entity:

- India and China, along with palm oil processors, refineries, and importers.

- Private equity funds.

- International palm oil investors and operators.

Scope of Work:

- Stakeholders collaborate to define demand and supply quantities, pricing structures, financial goals, and management objectives.

- End buyers specify their demand requirements.

- Private equity funds provide essential funding.

- Palm oil groups oversee plantation and mill operations.

The Unique Win-Win Model:

- End buyers have assurance regarding specific volumes and pricing structures.

- Producers work within predefined quantity and cost structures.

- Stakeholders share profits based on agreed-upon conditions.

- Private equity fund investors have confidence in achieving business and financial expectations.

This unique business model emphasizes collaboration and alignment of goals among stakeholders, creating a mutually beneficial and sustainable approach to the palm oil industry.

Palm Oil Business Model

9.0 Key Success Factors & Risk Mitigation

9.1 Key Success Factors:

- Certifications: Obtaining domestic, RSPO (Roundtable on Sustainable Palm Oil), and other international certifications is essential. These certifications demonstrate a commitment to sustainable and responsible palm oil production, which is increasingly important to consumers and regulators.

- Target Market Commitment: Building partnerships with processors from India and China who are committed to investing in Borneo to achieve food security in edible oil is critical. These partnerships ensure a stable market for the produced palm oil.

- Secure Funding: Having a secure and sustainable source of funding is paramount. Scalable funding options that allow for expansion as the project grows are essential for long-term success.

- Effective Entry Strategy: The acquisition of an existing palm oil plantation with a CPO mill is identified as the most effective method for rapid market penetration. This strategy provides immediate access to infrastructure and cash flow.

- Strong Management Team: A capable and experienced management team is crucial. Operational experience and an extensive network within the palm oil industry can help navigate challenges and seize opportunities effectively.

Sustainable Palm Oil is the key success factor

https://cdn.cdp.net/cdp-production/cms/reports/documents/000/006/522/original/CDP_Palm_Oil_Report_2022_Final.pdf?1660821343

9.2 Risks:

In the palm oil industry, several risks and challenges must be considered:

- Environmental Opposition: Growing opposition to the use of palm oil due to its association with rainforest destruction poses a significant risk to the industry’s reputation and market access.

- Labour Dependence: The industry relies heavily on labour-intensive practices, and there is a lack of succession planning for the replacement of retiring farmworkers.

- Technological Gaps: The palm oil industry lags behind in adopting modern technology and equipment for harvesting and processing.

- Commodity Price Fluctuations: The industry is susceptible to price fluctuations in the commodity market, impacting profitability.

- Extraction Rate: The efficiency of palm oil extraction can vary, affecting overall production and revenue.

- Environmental Pollution: The palm oil mill effluent can lead to pollution, posing environmental and regulatory risks.

- High-Yield Varieties: Research and development (R&D) efforts are needed to develop high-yield, disease-resistant palm oil varieties.

9.3 Risk Mitigation:

To address these risks, several mitigation strategies can be implemented:

- Sustainable Practices: The establishment of organizations like The Roundtable on Sustainable Palm Oil (RSPO) promotes sustainable palm oil production. Adhering to sustainability standards and the NDPE policies (no deforestation, no peat development, and no exploitation) benefits local communities, the environment, and profitability.

- Technology Adoption: Collaborate with international groups to develop and implement modern farming and processing equipment and techniques. Encourage innovation and technology adoption within the industry.

- Joint Ventures: Consider joint venture or partnership investments in the upstream and midstream segments to secure contractual commitments to production and pricing strategies, reducing exposure to commodity price fluctuations.

- Efficiency Improvements: Upgrade processing equipment to improve the palm oil extraction rate and implement waste control processes to reduce pollution from palm oil mill effluent.

- R&D Investment: Commit to research and development efforts aimed at creating high-yield, nutritionally rich, disease-resistant, and pest-resistant oil palm varieties.

By proactively addressing these risks and implementing mitigation measures, the palm oil industry can enhance its sustainability, productivity, and resilience in the face of challenges.

10.0 Exit Strategy

Having a well-defined exit strategy is crucial for any business venture. Here are the proposed forms of exit, the benefits of the business to new investors, the attraction of the business to potential investors, and the winning strategy:

10.1 Forms of Exit:

- IPO (Initial Public Offering): Investors can exit by selling their shares as part of an IPO to the public.

- M&A (Merger and Acquisition): The business could be acquired by another company in a similar industry.

- Sale: Private investors may sell their shares to another private equity firm.

- Buyback: The company’s management may choose to repurchase the equity stake from private investors.

10.2 Benefits of the Business to New Investors:

For potential new investors, the business offers several advantages:

- Market: The target markets for products are processors and refineries in India and China, and these buyers are already part of the investment group in the entity.

- Revenue: The business generates recurring revenue with planned future growth.

- Price Stability: It provides a stable income that is competitive with other edible oils, such as soybean oil.

- Risk Reduction: The secure demand and price structure reduce risk exposure to commodity price fluctuations.

- Product Expansion: There is potential for expanding into new product lines, particularly downstream palm oil derivatives, offering additional revenue streams.

- Opportunity: Investors can capture the opportunity presented by new downstream products and increase additional revenue.

- Exit Timing: Exit can occur after the third year when the production cycle and cash flow stabilize. Longer investment periods generate greater revenue and higher returns.

10.3 Attraction of the Business to New Investors:

This business presents several attractive aspects for potential investors:

- Market Expansion: Investors can capture additional market share in the India and China edible oil industry.

- Cost Reduction: Acquisition opportunities can provide the chance to reduce costs and improve overall performance.

- Ebitda Improvement: Strategic alliances between production and retail channels can capture competitive advantages of vertical integration and enhance the bottom line.

- Leadership: New leadership teams can improve business and operational performance.

- Distribution Channels: The business offers access to new markets, products, and distribution channels.

- Revenue Growth: Potential for additional revenue with downstream palm oil products.

10.4 Winning Strategy:

The winning strategies for this business include:

- Vertical Integration: Implement a vertical integration model and form business alliances with stakeholders.

- Strong Management: Assemble a powerful management team with top global players to enhance high-quality management practices and profitable operations.

- Win-Win: Achieve a profitable business model that simultaneously addresses the needs of developing communities by providing affordable cooking oil and protects wildlife, especially pygmy elephants, from poaching, culling, and poisoning in unsustainable palm oil plantations.

By executing these strategies and highlighting the business’s positive impact on society and the environment, the business can achieve success and attract potential investors.